Practical Tax Consulting 2025: Focusing on Law

|

Description

Book Introduction

Fully reflects the 2025 revised tax law!

The last 1% that captures a customer's heart is not information, but speaking skills!

Practical conversation techniques that reflect real-life situations in the sales field!

Here are the key changes in the latest tax law for 2025:

First, the scope of gift-giving through transactions with specific corporations has been expanded, and the scope of relatives to whom gift-giving property deductions apply has been rationalized.

Second, a new requirement for the CEO to be in office was added to the special tax exemption for gift tax on business succession, and the scope of business-unrelated assets for the corporate business inheritance deduction and special tax exemption for gift tax on business succession was adjusted.

Third, the scope of assets subject to capital gains tax carryforward taxation has been expanded, and the abolition of financial investment income tax and the postponement of virtual asset taxation have been decided.

Recently, concerns about a global trade war and a prolonged economic downturn have made business management difficult.

Companies that have adequately improved their financial structure and secured liquidity will be able to cope, but those that have not are facing significant difficulties.

The same goes for tax administration.

If you miss the right timing for donations or are negligent in managing retained earnings, you may face major tax problems in the future.

If you are doing corporate business, you must review these aspects and prepare countermeasures.

Corporate sales is a completely different field from general insurance sales.

Proper consulting is only possible if you fully understand the legal and tax information required for a corporation.

But will sales be smooth sailing simply by having a wealth of knowledge and information? No.

No matter how vast the data, it is useless if it cannot persuade customers.

Sales is ultimately about winning over customers' hearts in order to sell products.

Moreover, corporate sales requires dealing with much more demanding and demanding clients.

You need to deliver the information that corporate CEOs need but don't know in a refined and fluent manner to hit the final 1%, the finishing touch.

『Practical Tax Consulting for Corporate Law-Centered Businesses』 provides the knowledge and speaking skills needed for this purpose.

By familiarizing yourself with the tax information contained in this book and reading and practicing the "Practical Speaking" that reflects real-world situations, you will gain confidence in your ability to succeed in sales.

The last 1% that captures a customer's heart is not information, but speaking skills!

Practical conversation techniques that reflect real-life situations in the sales field!

Here are the key changes in the latest tax law for 2025:

First, the scope of gift-giving through transactions with specific corporations has been expanded, and the scope of relatives to whom gift-giving property deductions apply has been rationalized.

Second, a new requirement for the CEO to be in office was added to the special tax exemption for gift tax on business succession, and the scope of business-unrelated assets for the corporate business inheritance deduction and special tax exemption for gift tax on business succession was adjusted.

Third, the scope of assets subject to capital gains tax carryforward taxation has been expanded, and the abolition of financial investment income tax and the postponement of virtual asset taxation have been decided.

Recently, concerns about a global trade war and a prolonged economic downturn have made business management difficult.

Companies that have adequately improved their financial structure and secured liquidity will be able to cope, but those that have not are facing significant difficulties.

The same goes for tax administration.

If you miss the right timing for donations or are negligent in managing retained earnings, you may face major tax problems in the future.

If you are doing corporate business, you must review these aspects and prepare countermeasures.

Corporate sales is a completely different field from general insurance sales.

Proper consulting is only possible if you fully understand the legal and tax information required for a corporation.

But will sales be smooth sailing simply by having a wealth of knowledge and information? No.

No matter how vast the data, it is useless if it cannot persuade customers.

Sales is ultimately about winning over customers' hearts in order to sell products.

Moreover, corporate sales requires dealing with much more demanding and demanding clients.

You need to deliver the information that corporate CEOs need but don't know in a refined and fluent manner to hit the final 1%, the finishing touch.

『Practical Tax Consulting for Corporate Law-Centered Businesses』 provides the knowledge and speaking skills needed for this purpose.

By familiarizing yourself with the tax information contained in this book and reading and practicing the "Practical Speaking" that reflects real-world situations, you will gain confidence in your ability to succeed in sales.

index

preface

Part 1.

Developing knowledge

Topic 01.

Corporations and Financial Statements

Ⅰ.

Topic Introduction

Ⅱ.

Key Summary

1.

Understanding the Corporate Market

2.

Key Consulting Issues

3.

How to understand financial information

4.

Types of financial statements

5.

financial statements

6.

Income statement

7.

Statement of changes in equity, statement of appropriation of retained earnings, statement of cash flows

8.

External audit company financial statements vs.

General corporate financial statements

Topic 02.

Key concepts of tax law

Ⅰ.

Topic Introduction

Ⅱ.

Key Summary

1.

Types of national and local taxes

2.

Preclusion period and statute of limitations

3.

Secondary tax obligations of investors

4.

Amendment report, late report, correction request

5.

Surtax

6.

Scope of special related persons

Topic 03.

Corporate tax and income tax system

Ⅰ.

Topic Introduction

Ⅱ.

Key Summary

1.

Corporate tax vs.

income tax

2.

Corporate tax system and tax adjustment

3.

Tax deductions and reductions

4.

Types of income taxed under the Income Tax Act

5.

Tax exemption, separate taxation, classified taxation, comprehensive taxation

6.

Income tax system: comprehensive income, retirement income, and capital gains

7.

Four major insurance premiums for employees (as of 2020)

Topic 04.

Inheritance tax and gift tax system

Ⅰ.

Topic Introduction

Ⅱ.

Key Summary

1.

Key provisions of the Civil Code regarding inheritance

2.

Comparison of inheritance tax and gift tax

3.

Inheritance tax system

4.

Gift tax system

5.

Property valuation methods

6.

Inheritance tax saving measures

Topic 05.

Corporate law and joint stock companies

Ⅰ.

Topic Introduction

Ⅱ.

Key Summary

1.

Types and characteristics of companies under commercial law

2.

Procedures for establishing a stock company

3.

stocks

4.

Shareholder

5.

Institutions (general meeting of shareholders, board of directors, auditors)

6.

Compensation for directors and auditors

7.

Special provisions for small-scale joint-stock companies with capital of less than 1 billion won

8.

Key points of the limited company

Part 2.

Practical speaking skills

Part 1: Income Planning

Topic 06. Start by reviewing CEO salaries and retirement benefits.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Compensation of each legally required executive officer

- Checkpoint 2: Example of the Effect of a Salary Increase

- Checkpoint 3: Tax limits on executive severance pay

- Checkpoint 4: Taxation of reconverting the executive salary system to a retirement allowance system

Ⅲ.

Concluding the topic

Topic 07.

Revise the corporation's articles of incorporation.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Key items in the Articles of Incorporation

- Checkpoint 2: Procedures for Amending the Articles of Incorporation of a Stock Company and Registration Information

Ⅲ.

Concluding the topic

Topic 08.

Use dividends appropriately

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

Checkpoint 1: Summary of Dividend Regulations under the Commercial Act

- Checkpoint 2: Adjustment of double taxation on dividend income

Ⅲ.

Concluding the topic

Topic 09.

Retained earnings can be released through profit burn.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

Checkpoint 1: Overview of Profit Burn Utilization

- Checkpoint 2: Spouse, etc. carryover tax

- Checkpoint 3: Procedures for acquiring and burning treasury stock under the Commercial Act

- Checkpoint 4: Acquisition of treasury stock and repayment of dividends

Ⅲ.

Concluding the topic

Topic 10.

Take sufficient time to resolve the debt.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Tax disadvantages of deferred payments

Checkpoint 2: Summary of Solutions to the Unpaid Payment Problem

Ⅲ.

Concluding the topic

Topic 11.

Use patent assignments with caution.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Tax and tax savings from patent transfer

Checkpoint 2: Key Tax Issues When Transferring Patent Rights

Ⅲ.

Concluding the topic

Topic 12.

Use capital reserve reduction dividends

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Capital Reserve Reduction Dividend

- Checkpoint 2: Laws and Regulations Related to Capital Reserve Reduction Dividends

Ⅲ.

Concluding the topic

Part 2: Stock Movement

Topic 13.

Understand the importance and methods of evaluating unlisted stocks.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: How to Value Unlisted Stocks for Tax Purposes

Checkpoint 2: Unlisted Stock Valuation Case

- Checkpoint 3: Tax Calculation Examples for Inheritance, Gift, and Transfer of Stocks

Ⅲ.

Concluding the topic

Topic 14.

Return the nominal trust shares to the actual owner.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

Checkpoint 1: Tax Obligations of Majority Shareholders and Risks of Nominee Trust Shares

Checkpoint 2: Solutions for Trusted Shares

- Checkpoint 3: System for verifying the actual owner of nominal trust stocks/Gift agenda for nominal trust stocks

Ⅲ.

Concluding the topic

Topic 15.

Low and high price transactions may be subject to gift tax.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Stock transfer price and special related party under tax law

- Checkpoint 2: Resolving trust holdings through acquisition of treasury stocks

Ⅲ.

Concluding the topic

Topic 16.

Make proper use of the business succession support system.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

Checkpoint 1: Overview of the Business Inheritance Deduction System

- Checkpoint 2: Special Taxation System for Gift Tax on Business Succession

Checkpoint 3: Special Taxation System for Gift Tax on Startup Funds

- Checkpoint 4: Special provisions for deferred payment for business succession

- Checkpoint 5: Inheritance tax (gift tax) payment deferral upon business succession

Ⅲ.

Concluding the topic

Part 3: Incorporation

Topic 17.

Propose corporate conversion to customers subject to honest reporting.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Criteria for those subject to honest reporting

- Checkpoint 2: Corporate vs.

Comparison of taxes for individual business owners

- Checkpoint 3: Incorporation Procedures

- Checkpoint 4: Decision-making process for corporate conversion

Ⅲ.

Concluding the topic

Topic 18.

It is relatively easy for self-employed individuals without real estate to convert to a corporation.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Tax savings through transfer of goodwill

- Checkpoint 2: Related regulations

Ⅲ.

Concluding the topic

Topic 19.

If you have real estate, convert it to a corporation to receive tax relief.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Transfer income tax carryover upon conversion to a corporation

- Checkpoint 2: Comparison of in-kind contribution and comprehensive business acquisition

- Checkpoint 3: Regulations related to tax reduction and comprehensive transfer of tax reduction and tax reduction in kind contribution

Ⅲ.

Concluding the topic

Part 4: Real Estate Corporations

Topic 20.

Tax savings are possible by using a real estate corporation.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Differences between sole proprietorships and corporations

- Checkpoint 2: Corporate Real Estate Acquisition Tax

- Checkpoint 3: Tax Comparison of Rental Income and Transfer Income (Individual vs.

corporation)

Ⅲ.

Concluding the topic

Topic 21.

Use the funds for a specific corporation

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Deposits and Interest Income

- Checkpoint 2: Gift of profits through transactions with specific corporations (Article 45-5 of the Capital Gains and Losses Act)

Ⅲ.

Concluding the topic

Topic 22.

Use excess dividends to pay out to specific corporations.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Exclusion of dividend income from income

- Checkpoint 2: Cases of Excessive Dividends by Specific Corporations

Ⅲ.

Concluding the topic

Topic 23.

Donate real estate to a specific corporation

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Personal Gifts vs.

Comparison of corporate gift tax burdens

- Checkpoint 2: Standards for gifting profits through transactions with specific corporations

Ⅲ.

Concluding the topic

Topic 24.

Use the in-house employee welfare fund.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Tax-saving effects of the in-house employee welfare fund

- Checkpoint 2: Target and Business of the In-House Employee Welfare Fund

Ⅲ.

Concluding the topic

Part 3.

Use of insurance

Topic 25.

Hedge your business risks with life insurance.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Acceptance and renunciation of inheritance

- Checkpoint 2: Inheritance tax reporting deadline and tax burden

Checkpoint 3: Risk Management and Funding Using Corporate Insurance Contracts

Ⅲ.

Concluding the topic

Topic 26. Choose the Right Financial Product for Your CEO's Severance Pay

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

Checkpoint 1: Understanding the Retirement Pension System

- Checkpoint 2: Taxation when withdrawing retirement pension

- Checkpoint 3: Securing retirement funds (retirement pension vs.

Insurance products)

Ⅲ.

Concluding the topic

Topic 27.

If you are a married couple or a business partner, use corporate cross-contracts.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Example of Inheritance Tax Calculation for You and Your Spouse

- Checkpoint 2: Cross-corporate contract between husband and wife executives

- Checkpoint 3: Cross-incorporation agreement between business partners

Ⅲ.

Concluding the topic

Topic 28.

Pay the insurance contract in kind

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Provisions related to dividends in kind under the Commercial Act

- Checkpoint 2: Tax-saving effects of dividends in kind

Ⅲ.

Concluding the topic

Topic 29.

If you treat insurance premiums as expenses, the corporate tax deferral effect occurs.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Tax Treatment of Insurance Premium Payments

- Checkpoint 2: Accounting for each insurance contract stage

- Checkpoint 3: Tax treatment when paying in kind for insurance contracts

- Checkpoint 4: Expense treatment of term insurance premiums

Ⅲ.

Concluding the topic

Topic 30.

Take advantage of tax-exempt life insurance profits.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

Checkpoint 1: Summary of Insurance Profit Tax Exemption Requirements

- Checkpoint 2: Time deposit vs.

Examples of tax-saving effects of whole life insurance

- Checkpoint 3: Tax Exemption of Short-Term, Low-Cancelation Whole Life Insurance

Ⅲ.

Concluding the topic

Topic 31.

Take advantage of the three major life insurance plans.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

Checkpoint 1: Overview and Benefits of the Three Major Whole Life Insurance Plans

- Checkpoint 2: Tax-saving effects of the three major plans (1) - Generation-skipping inheritance effect

- Checkpoint 3: Tax-saving effects of the three major plans (2) - Income tax and inheritance tax exemption effects

Ⅲ.

Concluding the topic

Topic 32.

When signing up for corporate group insurance, accounting and tax processing are as follows.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Tax treatment of group insurance with the contracting corporation, insured employees, and beneficiary corporation.

- Checkpoint 2: Scope of earned income

Ⅲ.

Concluding the topic

supplement

[Appendix 1] Major tax deductions and reductions under the Special Tax Exceptions and Restrictions Act

1.

Tax reduction for startups, small and medium-sized enterprises, etc.

2.

Special tax reduction for small and medium-sized enterprises

3.

Tax deduction for research personnel development expenses

4.

Tax deduction for performance-based bonuses for small and medium-sized enterprises (SMEs) that share performance

5.

Integrated Investment Tax Credit

6.

Tax credits for companies that increase earned income

7.

Integrated Employment Tax Credit

8.

Special taxation for small and medium-sized enterprises that maintain employment

[Appendix 2] Relevant industries of small and medium-sized enterprises eligible for the business inheritance deduction/business succession gift tax exemption

1.

Industry according to the Korean Standard Industrial Classification

2.

Industry according to the provisions of individual laws

Part 1.

Developing knowledge

Topic 01.

Corporations and Financial Statements

Ⅰ.

Topic Introduction

Ⅱ.

Key Summary

1.

Understanding the Corporate Market

2.

Key Consulting Issues

3.

How to understand financial information

4.

Types of financial statements

5.

financial statements

6.

Income statement

7.

Statement of changes in equity, statement of appropriation of retained earnings, statement of cash flows

8.

External audit company financial statements vs.

General corporate financial statements

Topic 02.

Key concepts of tax law

Ⅰ.

Topic Introduction

Ⅱ.

Key Summary

1.

Types of national and local taxes

2.

Preclusion period and statute of limitations

3.

Secondary tax obligations of investors

4.

Amendment report, late report, correction request

5.

Surtax

6.

Scope of special related persons

Topic 03.

Corporate tax and income tax system

Ⅰ.

Topic Introduction

Ⅱ.

Key Summary

1.

Corporate tax vs.

income tax

2.

Corporate tax system and tax adjustment

3.

Tax deductions and reductions

4.

Types of income taxed under the Income Tax Act

5.

Tax exemption, separate taxation, classified taxation, comprehensive taxation

6.

Income tax system: comprehensive income, retirement income, and capital gains

7.

Four major insurance premiums for employees (as of 2020)

Topic 04.

Inheritance tax and gift tax system

Ⅰ.

Topic Introduction

Ⅱ.

Key Summary

1.

Key provisions of the Civil Code regarding inheritance

2.

Comparison of inheritance tax and gift tax

3.

Inheritance tax system

4.

Gift tax system

5.

Property valuation methods

6.

Inheritance tax saving measures

Topic 05.

Corporate law and joint stock companies

Ⅰ.

Topic Introduction

Ⅱ.

Key Summary

1.

Types and characteristics of companies under commercial law

2.

Procedures for establishing a stock company

3.

stocks

4.

Shareholder

5.

Institutions (general meeting of shareholders, board of directors, auditors)

6.

Compensation for directors and auditors

7.

Special provisions for small-scale joint-stock companies with capital of less than 1 billion won

8.

Key points of the limited company

Part 2.

Practical speaking skills

Part 1: Income Planning

Topic 06. Start by reviewing CEO salaries and retirement benefits.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Compensation of each legally required executive officer

- Checkpoint 2: Example of the Effect of a Salary Increase

- Checkpoint 3: Tax limits on executive severance pay

- Checkpoint 4: Taxation of reconverting the executive salary system to a retirement allowance system

Ⅲ.

Concluding the topic

Topic 07.

Revise the corporation's articles of incorporation.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Key items in the Articles of Incorporation

- Checkpoint 2: Procedures for Amending the Articles of Incorporation of a Stock Company and Registration Information

Ⅲ.

Concluding the topic

Topic 08.

Use dividends appropriately

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

Checkpoint 1: Summary of Dividend Regulations under the Commercial Act

- Checkpoint 2: Adjustment of double taxation on dividend income

Ⅲ.

Concluding the topic

Topic 09.

Retained earnings can be released through profit burn.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

Checkpoint 1: Overview of Profit Burn Utilization

- Checkpoint 2: Spouse, etc. carryover tax

- Checkpoint 3: Procedures for acquiring and burning treasury stock under the Commercial Act

- Checkpoint 4: Acquisition of treasury stock and repayment of dividends

Ⅲ.

Concluding the topic

Topic 10.

Take sufficient time to resolve the debt.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Tax disadvantages of deferred payments

Checkpoint 2: Summary of Solutions to the Unpaid Payment Problem

Ⅲ.

Concluding the topic

Topic 11.

Use patent assignments with caution.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Tax and tax savings from patent transfer

Checkpoint 2: Key Tax Issues When Transferring Patent Rights

Ⅲ.

Concluding the topic

Topic 12.

Use capital reserve reduction dividends

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Capital Reserve Reduction Dividend

- Checkpoint 2: Laws and Regulations Related to Capital Reserve Reduction Dividends

Ⅲ.

Concluding the topic

Part 2: Stock Movement

Topic 13.

Understand the importance and methods of evaluating unlisted stocks.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: How to Value Unlisted Stocks for Tax Purposes

Checkpoint 2: Unlisted Stock Valuation Case

- Checkpoint 3: Tax Calculation Examples for Inheritance, Gift, and Transfer of Stocks

Ⅲ.

Concluding the topic

Topic 14.

Return the nominal trust shares to the actual owner.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

Checkpoint 1: Tax Obligations of Majority Shareholders and Risks of Nominee Trust Shares

Checkpoint 2: Solutions for Trusted Shares

- Checkpoint 3: System for verifying the actual owner of nominal trust stocks/Gift agenda for nominal trust stocks

Ⅲ.

Concluding the topic

Topic 15.

Low and high price transactions may be subject to gift tax.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Stock transfer price and special related party under tax law

- Checkpoint 2: Resolving trust holdings through acquisition of treasury stocks

Ⅲ.

Concluding the topic

Topic 16.

Make proper use of the business succession support system.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

Checkpoint 1: Overview of the Business Inheritance Deduction System

- Checkpoint 2: Special Taxation System for Gift Tax on Business Succession

Checkpoint 3: Special Taxation System for Gift Tax on Startup Funds

- Checkpoint 4: Special provisions for deferred payment for business succession

- Checkpoint 5: Inheritance tax (gift tax) payment deferral upon business succession

Ⅲ.

Concluding the topic

Part 3: Incorporation

Topic 17.

Propose corporate conversion to customers subject to honest reporting.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Criteria for those subject to honest reporting

- Checkpoint 2: Corporate vs.

Comparison of taxes for individual business owners

- Checkpoint 3: Incorporation Procedures

- Checkpoint 4: Decision-making process for corporate conversion

Ⅲ.

Concluding the topic

Topic 18.

It is relatively easy for self-employed individuals without real estate to convert to a corporation.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Tax savings through transfer of goodwill

- Checkpoint 2: Related regulations

Ⅲ.

Concluding the topic

Topic 19.

If you have real estate, convert it to a corporation to receive tax relief.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Transfer income tax carryover upon conversion to a corporation

- Checkpoint 2: Comparison of in-kind contribution and comprehensive business acquisition

- Checkpoint 3: Regulations related to tax reduction and comprehensive transfer of tax reduction and tax reduction in kind contribution

Ⅲ.

Concluding the topic

Part 4: Real Estate Corporations

Topic 20.

Tax savings are possible by using a real estate corporation.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Differences between sole proprietorships and corporations

- Checkpoint 2: Corporate Real Estate Acquisition Tax

- Checkpoint 3: Tax Comparison of Rental Income and Transfer Income (Individual vs.

corporation)

Ⅲ.

Concluding the topic

Topic 21.

Use the funds for a specific corporation

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Deposits and Interest Income

- Checkpoint 2: Gift of profits through transactions with specific corporations (Article 45-5 of the Capital Gains and Losses Act)

Ⅲ.

Concluding the topic

Topic 22.

Use excess dividends to pay out to specific corporations.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Exclusion of dividend income from income

- Checkpoint 2: Cases of Excessive Dividends by Specific Corporations

Ⅲ.

Concluding the topic

Topic 23.

Donate real estate to a specific corporation

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Personal Gifts vs.

Comparison of corporate gift tax burdens

- Checkpoint 2: Standards for gifting profits through transactions with specific corporations

Ⅲ.

Concluding the topic

Topic 24.

Use the in-house employee welfare fund.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Tax-saving effects of the in-house employee welfare fund

- Checkpoint 2: Target and Business of the In-House Employee Welfare Fund

Ⅲ.

Concluding the topic

Part 3.

Use of insurance

Topic 25.

Hedge your business risks with life insurance.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Acceptance and renunciation of inheritance

- Checkpoint 2: Inheritance tax reporting deadline and tax burden

Checkpoint 3: Risk Management and Funding Using Corporate Insurance Contracts

Ⅲ.

Concluding the topic

Topic 26. Choose the Right Financial Product for Your CEO's Severance Pay

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

Checkpoint 1: Understanding the Retirement Pension System

- Checkpoint 2: Taxation when withdrawing retirement pension

- Checkpoint 3: Securing retirement funds (retirement pension vs.

Insurance products)

Ⅲ.

Concluding the topic

Topic 27.

If you are a married couple or a business partner, use corporate cross-contracts.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Example of Inheritance Tax Calculation for You and Your Spouse

- Checkpoint 2: Cross-corporate contract between husband and wife executives

- Checkpoint 3: Cross-incorporation agreement between business partners

Ⅲ.

Concluding the topic

Topic 28.

Pay the insurance contract in kind

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Provisions related to dividends in kind under the Commercial Act

- Checkpoint 2: Tax-saving effects of dividends in kind

Ⅲ.

Concluding the topic

Topic 29.

If you treat insurance premiums as expenses, the corporate tax deferral effect occurs.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Tax Treatment of Insurance Premium Payments

- Checkpoint 2: Accounting for each insurance contract stage

- Checkpoint 3: Tax treatment when paying in kind for insurance contracts

- Checkpoint 4: Expense treatment of term insurance premiums

Ⅲ.

Concluding the topic

Topic 30.

Take advantage of tax-exempt life insurance profits.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

Checkpoint 1: Summary of Insurance Profit Tax Exemption Requirements

- Checkpoint 2: Time deposit vs.

Examples of tax-saving effects of whole life insurance

- Checkpoint 3: Tax Exemption of Short-Term, Low-Cancelation Whole Life Insurance

Ⅲ.

Concluding the topic

Topic 31.

Take advantage of the three major life insurance plans.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

Checkpoint 1: Overview and Benefits of the Three Major Whole Life Insurance Plans

- Checkpoint 2: Tax-saving effects of the three major plans (1) - Generation-skipping inheritance effect

- Checkpoint 3: Tax-saving effects of the three major plans (2) - Income tax and inheritance tax exemption effects

Ⅲ.

Concluding the topic

Topic 32.

When signing up for corporate group insurance, accounting and tax processing are as follows.

Ⅰ.

Topic Introduction

Ⅱ.

Practical speaking skills

- Checkpoint 1: Tax treatment of group insurance with the contracting corporation, insured employees, and beneficiary corporation.

- Checkpoint 2: Scope of earned income

Ⅲ.

Concluding the topic

supplement

[Appendix 1] Major tax deductions and reductions under the Special Tax Exceptions and Restrictions Act

1.

Tax reduction for startups, small and medium-sized enterprises, etc.

2.

Special tax reduction for small and medium-sized enterprises

3.

Tax deduction for research personnel development expenses

4.

Tax deduction for performance-based bonuses for small and medium-sized enterprises (SMEs) that share performance

5.

Integrated Investment Tax Credit

6.

Tax credits for companies that increase earned income

7.

Integrated Employment Tax Credit

8.

Special taxation for small and medium-sized enterprises that maintain employment

[Appendix 2] Relevant industries of small and medium-sized enterprises eligible for the business inheritance deduction/business succession gift tax exemption

1.

Industry according to the Korean Standard Industrial Classification

2.

Industry according to the provisions of individual laws

Into the book

Although a CEO is an individual executive, he or she is often the owner-manager of a corporation when viewed broadly.

From a corporation's perspective, the salary paid to the CEO can be treated as an expense.

If a corporation has sufficient profit-generating and payment capabilities, it can justifiably pay more to its CEO, who contributes the most.

If the salary is set appropriately considering the size of the corporation's profits, the corporation can also reduce corporate tax.

★ Practical Speaking Techniques

CEO: But if you raise salaries, income tax and the four major insurance premiums will also go up, so wouldn't that be ineffective?

FP: Of course, if you raise salaries, your income tax and health insurance burden will increase slightly compared to now.

Instead, since the salary increase is treated as an expense by the corporation, it will not increase as much as you think.

Meanwhile, an appropriate salary increase can also prevent unnecessary overpayments.

Moreover, raising salaries can also decrease the value of the company's stock.

In other words, a pay raise may result in a slight increase in taxes in the short term, but it may result in greater tax savings in the long term.

CEO: Well, I guess.

Just hearing it makes me wonder how much of a tax-saving it is.

FP: Here's something I brought as an example.

If you were to increase the CEO's current annual salary of 84 million won to 120 million won, you'd think his tax burden would increase significantly. However, if you actually calculate it, you'll see that it's not that significant.

Although income tax and health insurance premiums increase, the net increase in tax burden considering income tax and corporate tax is approximately 5.56 million won, as the increase in salary and health insurance premiums is treated as additional expenses when calculating corporate tax.

The tax burden on the increase is approximately 15.4% (= 5.56 million won/36 million won).

In addition, there is an advantage in that if you raise your salary, the stock value under the Capital Gains Tax Act will also decrease, making it more advantageous when moving stocks.

---From "Topic 06. Check the CEO's salary and retirement benefits first"

Many small and medium-sized business CEOs still do not fully understand the meaning and necessity of articles of incorporation.

The articles of incorporation of a corporation are a required document that must be prepared upon establishment.

However, since there are many cases where people do not pay attention to it afterwards, it is necessary to reflect the relevant contents in the articles of incorporation when tax laws or commercial laws are changed.

In this case, the procedure for amending the articles of incorporation under the Commercial Act must be followed.

In particular, it is advisable to prevent tax risks that may arise in the future by detailing and clearly stipulating matters such as executive compensation regulations, executive retirement allowance regulations, executive bonus regulations, and executive survivor compensation regulations as separate provisions that are part of the articles of incorporation.

★ Practical Speaking Techniques

FP: I have carefully reviewed the articles of association you provided last time.

Based on what we've reviewed, I'd like to highlight a few key points.

?

CEO: The current articles of incorporation have only been revised to reflect changes in tax laws from several years ago, specifically regarding executive retirement benefits.

But is there any need to change the articles of association again?

FP: The Articles of Incorporation are the internal laws of the company.

There are no immediate problems with the current articles of incorporation.

However, the Articles of Incorporation contain various important matters of the company, such as executive salaries, bonuses, and retirement pay, as well as provisions for institutions such as the general shareholders' meeting, board of directors, and auditors, as well as matters related to major decision-making such as shareholder transfer, stock purchase options, and dividends.

Therefore, it is necessary to periodically check whether it is suitable for the company's circumstances.

Your company has been overhauled several years ago, but I'd like to suggest a better alternative in several areas.

CEO: I see.

What specific parts need maintenance?

FP: Yes, I will explain the current company articles of incorporation one by one.

First, looking at Article O, ‘Purpose’, it states that the company is engaged in the manufacture of electronic components and all related businesses.

But as far as I know, your company, in addition to manufacturing, also imports overseas parts and sells them domestically, and leases part of the headquarters building, right?

CEO: That's right.

Previously, we only manufactured, but now we also import and sell products for business diversification purposes.

And recently, we are leasing out the remaining space from the construction of a new headquarters building.

But does this really have to be stipulated in the articles of incorporation?

FP: If a new business is added, it needs to be stipulated in the Articles of Incorporation and added to the registration.

If you skip this procedure, it may lead to tax problems.

For example, if you lease real estate to another person without a real estate rental business in your articles of incorporation or registration, the leased real estate will be viewed as an asset unrelated to your business, which may result in tax disadvantages.

---「Topic 07.

From “Revise the Articles of Incorporation of the Corporation”

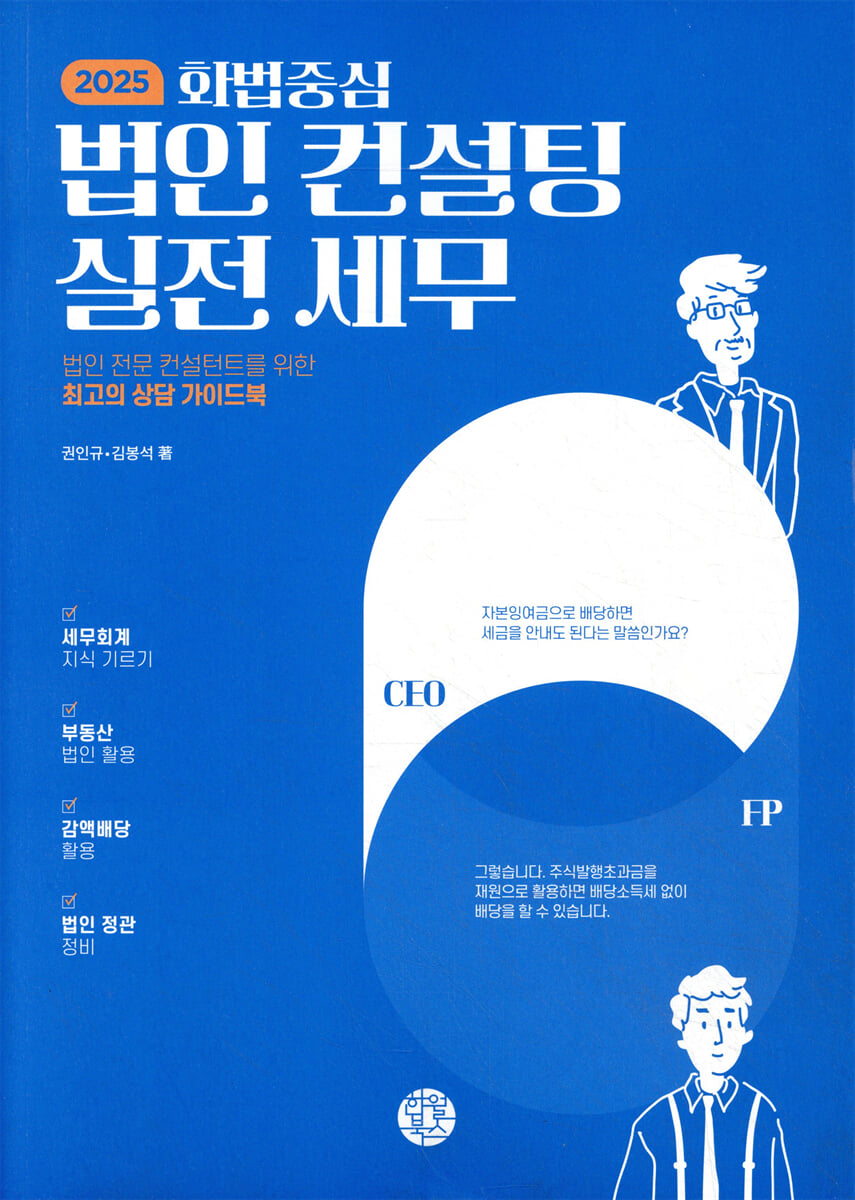

Although small and medium-sized businesses are increasingly actively paying dividends these days, many are still reluctant to do so due to the taxes they must pay.

Generally, if you use retained earnings to pay dividends, you must pay dividend income tax. However, if your financial income, including dividend income, exceeds 20 million won, your financial income is subject to comprehensive taxation, which can result in you paying a significant amount of tax and increasing your health insurance premium burden.

However, if dividends are paid using capital reserves such as excess stock issuance, there is no dividend income tax burden.

Therefore, corporations that have been reluctant to pay dividends due to tax reasons can now use this to pay dividends efficiently.

★ Practical Speaking Techniques

FP: As the surplus increases, the value of the company's stock increases, which can ultimately lead to significant taxes for the CEO, including inheritance and gift taxes.

Therefore, it is recommended to manage surplus through regular dividends even if there is some tax to pay.

By the way, did you receive any external investment a few years ago?

CEO: Yes, when business was difficult, we were fortunate enough to receive external investment and increase our capital.

If we hadn't received the investment at that time, we would have had to close down the company as I mentioned earlier.

From then on, the business started to do well little by little and we were able to pay dividends.

FP: I see.

The CEO just mentioned that he was concerned about paying dividends due to tax reasons. If there's a way to pay dividends without taxes, would you consider exploring it?

CEO: No, you're saying there's no tax on dividends? Our tax accountant says we have to pay a basic 15.4% tax, and if your annual dividend income exceeds 20 million won, you have to add up all your income for the year and re-report it.

FP: That's the general dividend.

By the way, have you ever heard of a capital reserve reduction dividend? Your company once received external investment and increased its capital by several dozen times its face value.

At this time, the difference between the stock issue price and the par value is indicated as stock issuance premium, as shown in the financial statements.

CEO: Oh, I remember.

Our par value was 5,000 won per share, but when we increased capital at that time, we issued the shares at around 100,000 won per share.

FP: Yes, the difference between the par value and the issue price, 95,000 won per share, is indicated as the stock issuance premium.

Using this as a resource, you can pay dividends without paying taxes.

This is called a capital reserve reduction dividend.

Here, capital reserve is a term from the Commercial Act, and in accounting terms, it can be considered to have a similar meaning to capital surplus.

In the past, capital reserves such as stock issuance premiums were, in principle, to be used to cover losses.

But 2011.

4. The Commercial Act was amended on 15th, allowing reserves exceeding 1.5 times the capital to be reduced at the general shareholders' meeting and to be distributed to shareholders as a source of income.

---「Topic 12.

From "Use the capital reserve reduction dividend"

Most of the corporations that FP meets are unlisted.

However, it is difficult to objectively measure the market value of unlisted companies because, except for some stocks, there are almost no transactions.

The tax law-regulated valuation method for unlisted stocks that reflects these points is called the supplementary valuation method.

Since the value calculated through the supplementary valuation method is the basis for calculating inheritance tax, gift tax, and capital gains tax, the valuation of unlisted stocks is a very important matter in evaluating the assets of a corporate CEO.

★ Practical Speaking Techniques

CEO: By the way, after hearing your story, I'm curious about the value of our company's stock.

FP: I thought you might be curious, so I roughly calculated the stock value based on the three-year tax adjustment statement you provided last week.

The face value per share is 10,000 won, but the current value per share is 580,000 won.

The total stock value is 5.8 billion won.

CEO: Is it really that high? Should I be happy that the tax law values our company so highly? The company's capital is 100 million won, and its current net assets are 4 billion won. How did it rise to 5.8 billion won? Is it because of the profit and loss ratio?

FP: Yes.

If you inherit now, the inheritance tax will be approximately 940 million won, if you make a gift, the gift tax will be 2.34 billion won, and if you transfer, the capital gains tax will be approximately 1.54 billion won (including local income tax).

CEO: You're saying I have to pay nearly 1 billion won in inheritance tax?

FP: Stock value is higher than expected because it is evaluated not only based on net assets (i.e. capital) but also takes into account profit and loss values.

That's why there are so many taxes.

CEO: I've been seeing a lot of news lately about people struggling with inheritance and gift taxes. After consulting with them myself, I've found out it's not a simple matter.

FP: So, you need to prepare various tax-saving methods, and also prepare for your children to pay their inheritance tax in cash.

If an unexpected problem arises when you are unprepared, your concerns may become reality.

---「Topic 13.

Understand the importance and method of evaluating unlisted stocks

Real estate accounts for a large portion of the assets of the wealthy in our country, exceeding 70%.

As the wealthy age, the need to pass on real estate to their children is also increasing.

However, since the real estate is often a large sum, the gift tax that must be paid is not insignificant.

Therefore, rather than gifting real estate directly to your children, you can reduce your children's gift tax burden by gifting it to a specific corporation in which your children are shareholders.

However, if a donation to a corporation meets certain requirements, gift tax may be imposed on shareholders of that specific corporation as well. Therefore, when providing consulting services to a corporation, it is essential to carefully consider the practical benefits.

★ Practical Speaking Techniques

FP: As the representative said, if you pay the gift tax on behalf of the other person, it is true that you will also have to pay additional gift tax.

If the real estate is worth 5 billion won, a 50% gift tax rate will apply, but if you pay taxes on top of that, you will have to pay an additional 50% gift tax.

CEO: So, we're still at a loss as to what to do.

Real estate prices keep rising, so I thought I would have to pay more taxes when I pass it on later, so I wanted to give it to him in advance.

FP: Yes. Then what about donating to a specific corporation? By "specific corporation," I mean a corporation in which your special relationship partner is a shareholder.

Simply put, you can think of it as a corporation in which the CEO's children are shareholders.

CEO: Yes, I guess you can think of it as a family corporation.

But, if I make a gift to a family corporation, will I be able to save on gift tax? Wouldn't that just be unnecessarily complicated?

FP: No.

Rather, it can save on gift tax that individuals have to pay.

Generally, when gifting real estate to a child, doesn't the recipient have to pay gift tax? Gift tax is levied at a maximum rate of 50% if the taxable value exceeds 3 billion won.

However, if you make a donation to a corporation where your child is a shareholder, corporate tax is imposed first. Generally, the corporate tax rate is 9% up to 200 million won, and 19% for the amount exceeding 200 million won up to 20 billion won.

And because it was a gift to a child corporation, it has the same effect as if it was transferred to the child.

---「Topic 23.

From "Donate real estate to a specific corporation"

Compared to mid-sized or large companies, most small and medium-sized companies have many shortcomings in terms of human resources and management systems, and are highly dependent on the CEO.

Therefore, if the CEO suddenly passes away, the company's existence could be in jeopardy.

To hedge against these risks, many small and medium-sized enterprises have recently been purchasing life insurance.

In order for a CEO or heir to receive a life insurance contract signed by a corporation or for an heir to receive insurance money, the corporation must have appropriate payment regulations in place.

Let's look at CEO legacy risk hedging, the essential and most important function of whole life insurance or term life insurance.

★ Practical Speaking Techniques

FP: I've met many CEOs in my career, and I've seen many cases where the CEO's death poses a risk to both the company and the bereaved family.

When a company's CEO suddenly dies, it becomes virtually impossible to maintain the company for a variety of reasons, starting with creditor issues. Don't you know that at a CEO's funeral, the first wreaths to arrive are those of creditors, and the debtors don't even show up?

CEO: That's the case for all small and medium-sized businesses like ours.

What other way is there?

FP: Usually, CEOs provide joint guarantees when their companies are facing difficulties or when they need to secure bank loans for new investments.

In this situation, the CEO's sudden death could lead to the company's bankruptcy, which could ultimately cause problems for the CEO's family.

Additionally, you must prepare for inheritance tax on the CEO's personal assets and company shares.

The valuation of company shares is done through the unlisted stock valuation method under tax law, and preparation for inheritance tax for business succession is also necessary.

CEO: Oh, but I've been running a business for 20 years, so I don't have any personal assets saved up.

It's stocks, I don't know how much they're worth, but if it becomes a problem later, can't we just gradually scale back the business? The economy isn't doing well these days.

Would there be any problem for a small company like ours?

FP: What the CEO said is not wrong.

However, if an unprepared accident occurs and the company is inherited without much knowledge, it can be painful for the remaining family members.

In some cases, corporate debts may be converted into personal debts of the surviving family members.

---「Topic 25.

From "Hedge your business risks with life insurance"

When running a business, accidents, big or small, can occur while employees are performing their duties.

Not only are injuries from machinery while working in a factory recognized as work-related accidents, but accidents that occur while commuting to and from work are also recognized as work-related accidents.

Many people subscribe to group insurance to prepare for such work-related accidents.

Group insurance is a contract in which the employer signs up under his or her name, while the insured group covers employees as a group. Recently, with the strengthening of the Serious Accident Punishment Act, the number of businesses signing up for the insurance has been increasing.

★ Practical Speaking Techniques

CEO: There's been a lot of talk lately about the Serious Disaster Punishment Act, so we're considering signing up for group insurance.

But if I sign up for group insurance, the company will have to pay the premium every month. Is there any advantage to this in terms of tax savings?

FP: Although group insurance isn't primarily intended for tax savings, since the company pays the premiums, treating this portion as an expense can also result in some corporate tax savings.

However, the cost processing differs depending on whether the beneficiary of the group insurance is an employee or a corporation.

CEO: Then what would be a better way?

FP: If the beneficiary is an employee, the insurance company will pay the accident insurance money directly to the employee when an insured accident occurs. If the beneficiary is a corporation, the accident insurance money will be received by the corporation.

Then, you can pay the insurance money received from the corporation to the relevant employee.

Usually, the beneficiary is more often a corporation.

This is because many CEOs prefer to have the company pay them out rather than having employees receive the money directly.

CEO: I see.

So, does tax treatment differ depending on who the beneficiary is?

FP: Yes.

First, I will explain the case where the beneficiary is a corporation, which is a form of membership that many corporations subscribe to.

In this case, when the corporation pays insurance premiums every month, the expired insurance premiums (business expenses + risk insurance premiums) are treated as expenses, and the accumulated insurance premiums that are refunded at maturity are treated as assets in the long-term financial product account.

And when a corporation receives insurance money due to an insured accident, it is processed as the corporation's income.

Of course, if you pay medical expenses and compensation to employees, this part can be processed as an expense.

From a corporation's perspective, the salary paid to the CEO can be treated as an expense.

If a corporation has sufficient profit-generating and payment capabilities, it can justifiably pay more to its CEO, who contributes the most.

If the salary is set appropriately considering the size of the corporation's profits, the corporation can also reduce corporate tax.

★ Practical Speaking Techniques

CEO: But if you raise salaries, income tax and the four major insurance premiums will also go up, so wouldn't that be ineffective?

FP: Of course, if you raise salaries, your income tax and health insurance burden will increase slightly compared to now.

Instead, since the salary increase is treated as an expense by the corporation, it will not increase as much as you think.

Meanwhile, an appropriate salary increase can also prevent unnecessary overpayments.

Moreover, raising salaries can also decrease the value of the company's stock.

In other words, a pay raise may result in a slight increase in taxes in the short term, but it may result in greater tax savings in the long term.

CEO: Well, I guess.

Just hearing it makes me wonder how much of a tax-saving it is.

FP: Here's something I brought as an example.

If you were to increase the CEO's current annual salary of 84 million won to 120 million won, you'd think his tax burden would increase significantly. However, if you actually calculate it, you'll see that it's not that significant.

Although income tax and health insurance premiums increase, the net increase in tax burden considering income tax and corporate tax is approximately 5.56 million won, as the increase in salary and health insurance premiums is treated as additional expenses when calculating corporate tax.

The tax burden on the increase is approximately 15.4% (= 5.56 million won/36 million won).

In addition, there is an advantage in that if you raise your salary, the stock value under the Capital Gains Tax Act will also decrease, making it more advantageous when moving stocks.

---From "Topic 06. Check the CEO's salary and retirement benefits first"

Many small and medium-sized business CEOs still do not fully understand the meaning and necessity of articles of incorporation.

The articles of incorporation of a corporation are a required document that must be prepared upon establishment.

However, since there are many cases where people do not pay attention to it afterwards, it is necessary to reflect the relevant contents in the articles of incorporation when tax laws or commercial laws are changed.

In this case, the procedure for amending the articles of incorporation under the Commercial Act must be followed.

In particular, it is advisable to prevent tax risks that may arise in the future by detailing and clearly stipulating matters such as executive compensation regulations, executive retirement allowance regulations, executive bonus regulations, and executive survivor compensation regulations as separate provisions that are part of the articles of incorporation.

★ Practical Speaking Techniques

FP: I have carefully reviewed the articles of association you provided last time.

Based on what we've reviewed, I'd like to highlight a few key points.

?

CEO: The current articles of incorporation have only been revised to reflect changes in tax laws from several years ago, specifically regarding executive retirement benefits.

But is there any need to change the articles of association again?

FP: The Articles of Incorporation are the internal laws of the company.

There are no immediate problems with the current articles of incorporation.

However, the Articles of Incorporation contain various important matters of the company, such as executive salaries, bonuses, and retirement pay, as well as provisions for institutions such as the general shareholders' meeting, board of directors, and auditors, as well as matters related to major decision-making such as shareholder transfer, stock purchase options, and dividends.

Therefore, it is necessary to periodically check whether it is suitable for the company's circumstances.

Your company has been overhauled several years ago, but I'd like to suggest a better alternative in several areas.

CEO: I see.

What specific parts need maintenance?

FP: Yes, I will explain the current company articles of incorporation one by one.

First, looking at Article O, ‘Purpose’, it states that the company is engaged in the manufacture of electronic components and all related businesses.

But as far as I know, your company, in addition to manufacturing, also imports overseas parts and sells them domestically, and leases part of the headquarters building, right?

CEO: That's right.

Previously, we only manufactured, but now we also import and sell products for business diversification purposes.

And recently, we are leasing out the remaining space from the construction of a new headquarters building.

But does this really have to be stipulated in the articles of incorporation?

FP: If a new business is added, it needs to be stipulated in the Articles of Incorporation and added to the registration.

If you skip this procedure, it may lead to tax problems.

For example, if you lease real estate to another person without a real estate rental business in your articles of incorporation or registration, the leased real estate will be viewed as an asset unrelated to your business, which may result in tax disadvantages.

---「Topic 07.

From “Revise the Articles of Incorporation of the Corporation”

Although small and medium-sized businesses are increasingly actively paying dividends these days, many are still reluctant to do so due to the taxes they must pay.

Generally, if you use retained earnings to pay dividends, you must pay dividend income tax. However, if your financial income, including dividend income, exceeds 20 million won, your financial income is subject to comprehensive taxation, which can result in you paying a significant amount of tax and increasing your health insurance premium burden.

However, if dividends are paid using capital reserves such as excess stock issuance, there is no dividend income tax burden.

Therefore, corporations that have been reluctant to pay dividends due to tax reasons can now use this to pay dividends efficiently.

★ Practical Speaking Techniques

FP: As the surplus increases, the value of the company's stock increases, which can ultimately lead to significant taxes for the CEO, including inheritance and gift taxes.

Therefore, it is recommended to manage surplus through regular dividends even if there is some tax to pay.

By the way, did you receive any external investment a few years ago?

CEO: Yes, when business was difficult, we were fortunate enough to receive external investment and increase our capital.

If we hadn't received the investment at that time, we would have had to close down the company as I mentioned earlier.

From then on, the business started to do well little by little and we were able to pay dividends.

FP: I see.

The CEO just mentioned that he was concerned about paying dividends due to tax reasons. If there's a way to pay dividends without taxes, would you consider exploring it?

CEO: No, you're saying there's no tax on dividends? Our tax accountant says we have to pay a basic 15.4% tax, and if your annual dividend income exceeds 20 million won, you have to add up all your income for the year and re-report it.

FP: That's the general dividend.

By the way, have you ever heard of a capital reserve reduction dividend? Your company once received external investment and increased its capital by several dozen times its face value.

At this time, the difference between the stock issue price and the par value is indicated as stock issuance premium, as shown in the financial statements.

CEO: Oh, I remember.

Our par value was 5,000 won per share, but when we increased capital at that time, we issued the shares at around 100,000 won per share.

FP: Yes, the difference between the par value and the issue price, 95,000 won per share, is indicated as the stock issuance premium.

Using this as a resource, you can pay dividends without paying taxes.

This is called a capital reserve reduction dividend.

Here, capital reserve is a term from the Commercial Act, and in accounting terms, it can be considered to have a similar meaning to capital surplus.

In the past, capital reserves such as stock issuance premiums were, in principle, to be used to cover losses.

But 2011.

4. The Commercial Act was amended on 15th, allowing reserves exceeding 1.5 times the capital to be reduced at the general shareholders' meeting and to be distributed to shareholders as a source of income.

---「Topic 12.

From "Use the capital reserve reduction dividend"

Most of the corporations that FP meets are unlisted.

However, it is difficult to objectively measure the market value of unlisted companies because, except for some stocks, there are almost no transactions.

The tax law-regulated valuation method for unlisted stocks that reflects these points is called the supplementary valuation method.

Since the value calculated through the supplementary valuation method is the basis for calculating inheritance tax, gift tax, and capital gains tax, the valuation of unlisted stocks is a very important matter in evaluating the assets of a corporate CEO.

★ Practical Speaking Techniques

CEO: By the way, after hearing your story, I'm curious about the value of our company's stock.

FP: I thought you might be curious, so I roughly calculated the stock value based on the three-year tax adjustment statement you provided last week.

The face value per share is 10,000 won, but the current value per share is 580,000 won.

The total stock value is 5.8 billion won.

CEO: Is it really that high? Should I be happy that the tax law values our company so highly? The company's capital is 100 million won, and its current net assets are 4 billion won. How did it rise to 5.8 billion won? Is it because of the profit and loss ratio?

FP: Yes.

If you inherit now, the inheritance tax will be approximately 940 million won, if you make a gift, the gift tax will be 2.34 billion won, and if you transfer, the capital gains tax will be approximately 1.54 billion won (including local income tax).

CEO: You're saying I have to pay nearly 1 billion won in inheritance tax?

FP: Stock value is higher than expected because it is evaluated not only based on net assets (i.e. capital) but also takes into account profit and loss values.

That's why there are so many taxes.

CEO: I've been seeing a lot of news lately about people struggling with inheritance and gift taxes. After consulting with them myself, I've found out it's not a simple matter.

FP: So, you need to prepare various tax-saving methods, and also prepare for your children to pay their inheritance tax in cash.

If an unexpected problem arises when you are unprepared, your concerns may become reality.

---「Topic 13.

Understand the importance and method of evaluating unlisted stocks

Real estate accounts for a large portion of the assets of the wealthy in our country, exceeding 70%.

As the wealthy age, the need to pass on real estate to their children is also increasing.

However, since the real estate is often a large sum, the gift tax that must be paid is not insignificant.

Therefore, rather than gifting real estate directly to your children, you can reduce your children's gift tax burden by gifting it to a specific corporation in which your children are shareholders.

However, if a donation to a corporation meets certain requirements, gift tax may be imposed on shareholders of that specific corporation as well. Therefore, when providing consulting services to a corporation, it is essential to carefully consider the practical benefits.

★ Practical Speaking Techniques

FP: As the representative said, if you pay the gift tax on behalf of the other person, it is true that you will also have to pay additional gift tax.

If the real estate is worth 5 billion won, a 50% gift tax rate will apply, but if you pay taxes on top of that, you will have to pay an additional 50% gift tax.

CEO: So, we're still at a loss as to what to do.

Real estate prices keep rising, so I thought I would have to pay more taxes when I pass it on later, so I wanted to give it to him in advance.

FP: Yes. Then what about donating to a specific corporation? By "specific corporation," I mean a corporation in which your special relationship partner is a shareholder.

Simply put, you can think of it as a corporation in which the CEO's children are shareholders.

CEO: Yes, I guess you can think of it as a family corporation.

But, if I make a gift to a family corporation, will I be able to save on gift tax? Wouldn't that just be unnecessarily complicated?

FP: No.

Rather, it can save on gift tax that individuals have to pay.

Generally, when gifting real estate to a child, doesn't the recipient have to pay gift tax? Gift tax is levied at a maximum rate of 50% if the taxable value exceeds 3 billion won.

However, if you make a donation to a corporation where your child is a shareholder, corporate tax is imposed first. Generally, the corporate tax rate is 9% up to 200 million won, and 19% for the amount exceeding 200 million won up to 20 billion won.

And because it was a gift to a child corporation, it has the same effect as if it was transferred to the child.

---「Topic 23.

From "Donate real estate to a specific corporation"

Compared to mid-sized or large companies, most small and medium-sized companies have many shortcomings in terms of human resources and management systems, and are highly dependent on the CEO.

Therefore, if the CEO suddenly passes away, the company's existence could be in jeopardy.

To hedge against these risks, many small and medium-sized enterprises have recently been purchasing life insurance.

In order for a CEO or heir to receive a life insurance contract signed by a corporation or for an heir to receive insurance money, the corporation must have appropriate payment regulations in place.

Let's look at CEO legacy risk hedging, the essential and most important function of whole life insurance or term life insurance.

★ Practical Speaking Techniques

FP: I've met many CEOs in my career, and I've seen many cases where the CEO's death poses a risk to both the company and the bereaved family.

When a company's CEO suddenly dies, it becomes virtually impossible to maintain the company for a variety of reasons, starting with creditor issues. Don't you know that at a CEO's funeral, the first wreaths to arrive are those of creditors, and the debtors don't even show up?

CEO: That's the case for all small and medium-sized businesses like ours.

What other way is there?

FP: Usually, CEOs provide joint guarantees when their companies are facing difficulties or when they need to secure bank loans for new investments.

In this situation, the CEO's sudden death could lead to the company's bankruptcy, which could ultimately cause problems for the CEO's family.

Additionally, you must prepare for inheritance tax on the CEO's personal assets and company shares.

The valuation of company shares is done through the unlisted stock valuation method under tax law, and preparation for inheritance tax for business succession is also necessary.

CEO: Oh, but I've been running a business for 20 years, so I don't have any personal assets saved up.

It's stocks, I don't know how much they're worth, but if it becomes a problem later, can't we just gradually scale back the business? The economy isn't doing well these days.

Would there be any problem for a small company like ours?

FP: What the CEO said is not wrong.

However, if an unprepared accident occurs and the company is inherited without much knowledge, it can be painful for the remaining family members.

In some cases, corporate debts may be converted into personal debts of the surviving family members.

---「Topic 25.

From "Hedge your business risks with life insurance"

When running a business, accidents, big or small, can occur while employees are performing their duties.

Not only are injuries from machinery while working in a factory recognized as work-related accidents, but accidents that occur while commuting to and from work are also recognized as work-related accidents.

Many people subscribe to group insurance to prepare for such work-related accidents.

Group insurance is a contract in which the employer signs up under his or her name, while the insured group covers employees as a group. Recently, with the strengthening of the Serious Accident Punishment Act, the number of businesses signing up for the insurance has been increasing.

★ Practical Speaking Techniques

CEO: There's been a lot of talk lately about the Serious Disaster Punishment Act, so we're considering signing up for group insurance.

But if I sign up for group insurance, the company will have to pay the premium every month. Is there any advantage to this in terms of tax savings?

FP: Although group insurance isn't primarily intended for tax savings, since the company pays the premiums, treating this portion as an expense can also result in some corporate tax savings.

However, the cost processing differs depending on whether the beneficiary of the group insurance is an employee or a corporation.

CEO: Then what would be a better way?

FP: If the beneficiary is an employee, the insurance company will pay the accident insurance money directly to the employee when an insured accident occurs. If the beneficiary is a corporation, the accident insurance money will be received by the corporation.

Then, you can pay the insurance money received from the corporation to the relevant employee.

Usually, the beneficiary is more often a corporation.

This is because many CEOs prefer to have the company pay them out rather than having employees receive the money directly.

CEO: I see.

So, does tax treatment differ depending on who the beneficiary is?

FP: Yes.

First, I will explain the case where the beneficiary is a corporation, which is a form of membership that many corporations subscribe to.

In this case, when the corporation pays insurance premiums every month, the expired insurance premiums (business expenses + risk insurance premiums) are treated as expenses, and the accumulated insurance premiums that are refunded at maturity are treated as assets in the long-term financial product account.

And when a corporation receives insurance money due to an insured accident, it is processed as the corporation's income.

Of course, if you pay medical expenses and compensation to employees, this part can be processed as an expense.

---「Topic 32.

From "Accounting and tax treatment when signing up for corporate group insurance"

From "Accounting and tax treatment when signing up for corporate group insurance"

Publisher's Review

There is no better practice than practice!

Conversation techniques that can be applied immediately in the field!

The core skills of corporate sales, condensed from the knowledge and experience of current experts!

Insurance sales involve selling intangible future value, and the product offerings are complex.

So, it is more important than anything to stimulate customer needs.

To achieve this, you must develop the ability to identify customer problems, master practical speaking skills according to the sales process, and demonstrate techniques for freely applying them.

Only then can we achieve the coveted fruit of concluding a contract.

Additionally, by learning practical speaking skills and immediately capturing the hearts of customers with logical and persuasive words, you can more easily achieve good results.

In other words, practical speaking is the best method to achieve maximum results with minimum effort and cost.

『Practical Tax Consulting for Corporate Law』 contains various information and speaking techniques necessary for corporate business.

There is a saying that “emotion comes from the details.”

To capture the hearts of customers and sell products, you need to pay attention to even the smallest details to impress them.

If you consistently practice practical speaking techniques developed by active professionals that reflect the specific situations in the field, they will become a key sales weapon.

Conversation techniques that can be applied immediately in the field!

The core skills of corporate sales, condensed from the knowledge and experience of current experts!

Insurance sales involve selling intangible future value, and the product offerings are complex.

So, it is more important than anything to stimulate customer needs.

To achieve this, you must develop the ability to identify customer problems, master practical speaking skills according to the sales process, and demonstrate techniques for freely applying them.

Only then can we achieve the coveted fruit of concluding a contract.

Additionally, by learning practical speaking skills and immediately capturing the hearts of customers with logical and persuasive words, you can more easily achieve good results.

In other words, practical speaking is the best method to achieve maximum results with minimum effort and cost.

『Practical Tax Consulting for Corporate Law』 contains various information and speaking techniques necessary for corporate business.

There is a saying that “emotion comes from the details.”

To capture the hearts of customers and sell products, you need to pay attention to even the smallest details to impress them.

If you consistently practice practical speaking techniques developed by active professionals that reflect the specific situations in the field, they will become a key sales weapon.

GOODS SPECIFICS

- Date of issue: June 25, 2025

- Page count, weight, size: 508 pages | 185*260*17mm

- ISBN13: 9791198637741

- ISBN10: 1198637749

You may also like

카테고리

korean

korean

![GQ KOREA Mark (Monthly): December [2025]](http://librairie.coreenne.fr/cdn/shop/files/8ef265dbbfbf186523ed75ba7319009d.jpg?v=1765340328&width=3840)