Accounting is money?

|

Description

Book Introduction

Proven by 『I almost worked without knowing accounting again!』

The best authors in accounting

Let's unfold the actual financial statements and interpret the 'language of money'!

***

"Even though I studied accounting, why am I still left with only question marks when I look at financial statements?" This book begins with that very question.

For those who are still stuck in their accounting studies despite their years of experience, the authors of "I Almost Got to Work Without Knowing Accounting Again!", which countless readers have chosen as the "Accounting Book of My Life," have taken up their pens again.

This time, it's not about theories, but about 'practical accounting' that applies directly to the field.

The reason we often fail at interpreting financial statements is because we miss the 'accounting context' hidden behind the numbers.

Financial statements are not simply tables of numbers.

It contains the company's strategy, management's judgment, and market changes.

Moreover, accounting treatments differ across industries, from how revenue is recognized to how cost structures are structured.

Financial statements can't be explained with a simple formula like, "High debt means poor performance." Why did investors cheer when SK Hynix's debt surged to nearly 3 trillion won? What is the significance of the over 10 trillion won in borrowings in Samsung Electronics' financial statements? When analyzing financial statements, it's important to understand the background and context behind the numbers, not just the numbers themselves.

Numbers are easily misinterpreted without understanding the accounting context.

When it comes to understanding accounting in context, there's no better resource than real-world examples. From SK Hynix to Today's House, the authors' over 100 case studies from business settings illustrate the vivid realities of the intertwining of accounting and management.

The new accounting standards (K-IFRS 18) will be fully implemented starting in 2027.

If Kakao's financial statements are adjusted according to K-IFRS 18, its 2023 performance will change from an operating profit of KRW 460.8 billion to an operating loss of KRW 1.4214 trillion! This book is the first accounting book to comprehensively analyze K-IFRS 18, which will revolutionize operating profit calculations.

When you study accounting through examples, numbers become stories, not codes.

Accounting is not simply a record-keeping tool; it shows the interactions between businesses, markets, capital, and people.

Reading financial statements well means understanding the context in which the numbers were created.

When we can read accounting as a story, we finally gain the ability to see through the 'flow of money'.

The best authors in accounting

Let's unfold the actual financial statements and interpret the 'language of money'!

***

"Even though I studied accounting, why am I still left with only question marks when I look at financial statements?" This book begins with that very question.

For those who are still stuck in their accounting studies despite their years of experience, the authors of "I Almost Got to Work Without Knowing Accounting Again!", which countless readers have chosen as the "Accounting Book of My Life," have taken up their pens again.

This time, it's not about theories, but about 'practical accounting' that applies directly to the field.

The reason we often fail at interpreting financial statements is because we miss the 'accounting context' hidden behind the numbers.

Financial statements are not simply tables of numbers.

It contains the company's strategy, management's judgment, and market changes.

Moreover, accounting treatments differ across industries, from how revenue is recognized to how cost structures are structured.

Financial statements can't be explained with a simple formula like, "High debt means poor performance." Why did investors cheer when SK Hynix's debt surged to nearly 3 trillion won? What is the significance of the over 10 trillion won in borrowings in Samsung Electronics' financial statements? When analyzing financial statements, it's important to understand the background and context behind the numbers, not just the numbers themselves.

Numbers are easily misinterpreted without understanding the accounting context.

When it comes to understanding accounting in context, there's no better resource than real-world examples. From SK Hynix to Today's House, the authors' over 100 case studies from business settings illustrate the vivid realities of the intertwining of accounting and management.

The new accounting standards (K-IFRS 18) will be fully implemented starting in 2027.

If Kakao's financial statements are adjusted according to K-IFRS 18, its 2023 performance will change from an operating profit of KRW 460.8 billion to an operating loss of KRW 1.4214 trillion! This book is the first accounting book to comprehensively analyze K-IFRS 18, which will revolutionize operating profit calculations.

When you study accounting through examples, numbers become stories, not codes.

Accounting is not simply a record-keeping tool; it shows the interactions between businesses, markets, capital, and people.

Reading financial statements well means understanding the context in which the numbers were created.

When we can read accounting as a story, we finally gain the ability to see through the 'flow of money'.

- You can preview some of the book's contents.

Preview

index

Preface _ What is Accounting? Accounting is Money!

[Special Feature] The upcoming K-IFRS 18 will drastically change the operating profit and loss in the income statement.

Lesson 01.

How do E-Mart and Gmarket calculate sales differently? Gross sales, net sales

Lesson 02.

Are the Big Three Luxury Platforms Really Being Overtaken by Latecomers? : Sales Comparisons Are Illusory

Lesson 03.

Unique Revenue Recognition in Shipbuilding and Construction Companies: Completion vs.

Progress criteria

Lesson 04.

Is Shinsegae Gangnam's sales figure really 3 trillion won? Sales on the income statement are different from GMV (gross merchandise value).

Lesson 05.

Cases of fraudulent accounting uncovered by the Financial Supervisory Service

Lesson 06.

Debt is debt! What's different about SK Hynix's "advance payment"?

Lesson 07.

The identity of the large debt on Megastudy's balance sheet: Sometimes it's advance payments, sometimes it's unearned revenue?

Lesson 08.

Why Airlines Plead: "Please Use Mileage": Deferred Revenue Liabilities

Lesson 09.

Naver's performance is the magic of 'depreciation'?

Lesson 10.

'EBITDA' commonly appears in articles from Kia, LG Ensol, SK Hynix, and Naver.

Lesson 11.

Why does HMM depreciate even the ships it leases?

Lesson 12.

Various intangible assets that become assets and then expenses

: Studio Dragon production costs, Gompyo trademark, daily instructor exclusive fee, etc.

Lesson 13.

Hyundai Motor Company's development cost exceeds 1 trillion won, while Sangsung Electronics' is at zero. The world of development cost accounting.

Lesson 14.

"The machine is not worth its price" Impairment accounting for tangible assets

Lesson 15.

The Gumdrop of M&A: Goodwill and PPA Amortization

Lesson 16.

PPA Lessons from E-Mart's Acquisition of Gmarket and Celltrion's Healthcare Merger

Lesson 17.

"I gave you credit, but I think it'll be canceled": Accounts Receivable Allowance Accounting

Lesson 18.

The stagnation of over 10 trillion won in debt on Samsung Electronics and Samsung Electronics' financial statements.

Lesson 19.

Oil companies cry and laugh under the inventory valuation method: Inventory unit valuation is important in the income statement.

Lesson 20.

When the value of inventory assets held rises or falls

Lesson 21.

Battery-Dead Inventory Valuations Save Semiconductors: Inventory Asset Losses and Refunds

Lesson 22.

Changes that appear in financial statements when increasing or decreasing capital

Lesson 23.

Why can we escape capital erosion by doing free potatoes?

Lesson 24.

Singapore Investment Corporation Recovers $4 Trillion in Building Investments: The Story of Paid-in Capital Increase

Lesson 25.

Hyundai and Kia's money-eating hippopotamus, 'engine recall reserves'... Goodbye now?

Lesson 26.

The unfortunate story of Kookbo Design, a "side-hustle genius": Accounting for stock investments for capital gains.

Lesson 27.

Progress-Based Construction Accounting: What if the Total Estimated Cost Changes During Construction?

Lesson 28.

The First Step to Lease Accounting: Understanding the Difference Between Financial and Operating Leases

Lesson 29.

Lease accounting has completely changed. Account for operating leases as if they were financial leases!

Lesson 30.

Asiana and HMM's debt ratios soar due to accounting fraud and lease accounting.

Lesson 31.

The inside story behind Homeplus selling and re-leasing real estate

Lesson 32.

Problems that practitioners dealing with lease accounting are likely to encounter

Lesson 33.

Why the Rising Stock Price Actually Worsens a Company's Income Statement

Lesson 34. Rhinos Missed Out on Billions of Won in IPO Profits Due to Unfamiliarity with CB Convertible Bond Accounting

Lesson 35.

With capital erosion of 800 billion won, was Today's House a doomed company?

Lesson 36.

Debt Securities, But Capital?: EcoPro BM and POSCO Future M's Perpetual Bonds (New Capital Securities)

Lesson 37.

Why Netmarble is smiling as water purifier and bidet rental furniture increases

Lesson 38.

The impact of equity method valuation differences and investment differences on equity method profits and losses

Lesson 39.

Why Yuhan Corporation's Consolidated and Separate Financial Statements Differ: Understanding and Using Consolidated Financial Statements

Lesson 40.

Non-controlling interests? The answer lies in the method of preparing consolidated financial statements.

Lesson 41.

Cash flow statement that complements the fatal flaws of accrual accounting

Lesson 42.

Cash Flow Traffic Lights: Which Companies to Invest in and Which to Avoid

Lesson 43.

The Cost of Petroleum Products: Awareness of the Cost of Petroleum Products While Grilling Samgyeopsal

[Special Feature] The upcoming K-IFRS 18 will drastically change the operating profit and loss in the income statement.

Lesson 01.

How do E-Mart and Gmarket calculate sales differently? Gross sales, net sales

Lesson 02.

Are the Big Three Luxury Platforms Really Being Overtaken by Latecomers? : Sales Comparisons Are Illusory

Lesson 03.

Unique Revenue Recognition in Shipbuilding and Construction Companies: Completion vs.

Progress criteria

Lesson 04.

Is Shinsegae Gangnam's sales figure really 3 trillion won? Sales on the income statement are different from GMV (gross merchandise value).

Lesson 05.

Cases of fraudulent accounting uncovered by the Financial Supervisory Service

Lesson 06.

Debt is debt! What's different about SK Hynix's "advance payment"?

Lesson 07.

The identity of the large debt on Megastudy's balance sheet: Sometimes it's advance payments, sometimes it's unearned revenue?

Lesson 08.

Why Airlines Plead: "Please Use Mileage": Deferred Revenue Liabilities

Lesson 09.

Naver's performance is the magic of 'depreciation'?

Lesson 10.

'EBITDA' commonly appears in articles from Kia, LG Ensol, SK Hynix, and Naver.

Lesson 11.

Why does HMM depreciate even the ships it leases?

Lesson 12.

Various intangible assets that become assets and then expenses

: Studio Dragon production costs, Gompyo trademark, daily instructor exclusive fee, etc.

Lesson 13.

Hyundai Motor Company's development cost exceeds 1 trillion won, while Sangsung Electronics' is at zero. The world of development cost accounting.

Lesson 14.

"The machine is not worth its price" Impairment accounting for tangible assets

Lesson 15.

The Gumdrop of M&A: Goodwill and PPA Amortization

Lesson 16.

PPA Lessons from E-Mart's Acquisition of Gmarket and Celltrion's Healthcare Merger

Lesson 17.

"I gave you credit, but I think it'll be canceled": Accounts Receivable Allowance Accounting

Lesson 18.

The stagnation of over 10 trillion won in debt on Samsung Electronics and Samsung Electronics' financial statements.

Lesson 19.

Oil companies cry and laugh under the inventory valuation method: Inventory unit valuation is important in the income statement.

Lesson 20.

When the value of inventory assets held rises or falls

Lesson 21.

Battery-Dead Inventory Valuations Save Semiconductors: Inventory Asset Losses and Refunds

Lesson 22.

Changes that appear in financial statements when increasing or decreasing capital

Lesson 23.

Why can we escape capital erosion by doing free potatoes?

Lesson 24.

Singapore Investment Corporation Recovers $4 Trillion in Building Investments: The Story of Paid-in Capital Increase

Lesson 25.

Hyundai and Kia's money-eating hippopotamus, 'engine recall reserves'... Goodbye now?

Lesson 26.

The unfortunate story of Kookbo Design, a "side-hustle genius": Accounting for stock investments for capital gains.

Lesson 27.

Progress-Based Construction Accounting: What if the Total Estimated Cost Changes During Construction?

Lesson 28.

The First Step to Lease Accounting: Understanding the Difference Between Financial and Operating Leases

Lesson 29.

Lease accounting has completely changed. Account for operating leases as if they were financial leases!

Lesson 30.

Asiana and HMM's debt ratios soar due to accounting fraud and lease accounting.

Lesson 31.

The inside story behind Homeplus selling and re-leasing real estate

Lesson 32.

Problems that practitioners dealing with lease accounting are likely to encounter

Lesson 33.

Why the Rising Stock Price Actually Worsens a Company's Income Statement

Lesson 34. Rhinos Missed Out on Billions of Won in IPO Profits Due to Unfamiliarity with CB Convertible Bond Accounting

Lesson 35.

With capital erosion of 800 billion won, was Today's House a doomed company?

Lesson 36.

Debt Securities, But Capital?: EcoPro BM and POSCO Future M's Perpetual Bonds (New Capital Securities)

Lesson 37.

Why Netmarble is smiling as water purifier and bidet rental furniture increases

Lesson 38.

The impact of equity method valuation differences and investment differences on equity method profits and losses

Lesson 39.

Why Yuhan Corporation's Consolidated and Separate Financial Statements Differ: Understanding and Using Consolidated Financial Statements

Lesson 40.

Non-controlling interests? The answer lies in the method of preparing consolidated financial statements.

Lesson 41.

Cash flow statement that complements the fatal flaws of accrual accounting

Lesson 42.

Cash Flow Traffic Lights: Which Companies to Invest in and Which to Avoid

Lesson 43.

The Cost of Petroleum Products: Awareness of the Cost of Petroleum Products While Grilling Samgyeopsal

Detailed image

Publisher's Review

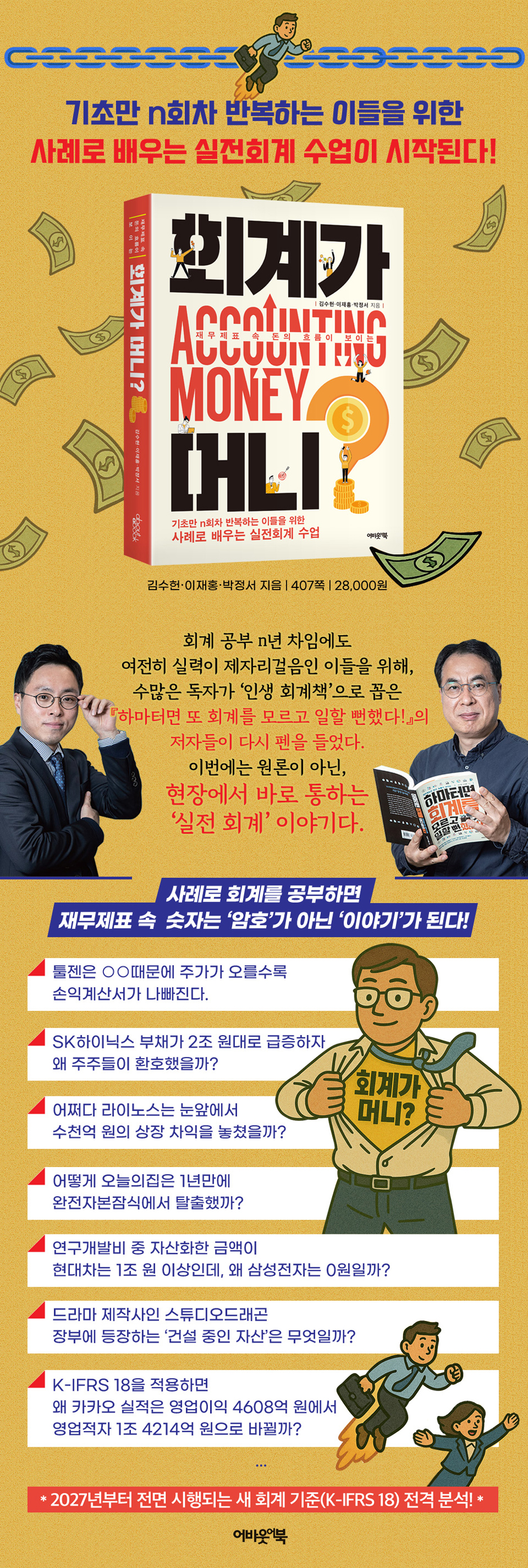

For those who repeat the basics n times

Practical Accounting Class: Learning through Case Studies

"Even though I studied accounting, why am I still left with only question marks when I look at financial statements?" This book begins with that very question.

For those who are still stuck in their accounting studies despite having studied them for years, the authors of "I Almost Got to Work Without Knowing Accounting Again!", which countless readers have chosen as the "accounting book of my life," have taken up their pens again.

This time, it's not about theories, but about 'practical accounting' that applies directly to the field.

The reason we often fail at interpreting financial statements is because we miss the 'accounting context' hidden behind the numbers.

Financial statements are not simply tables of numbers.

It contains the company's strategy, management's judgment, and market changes.

Moreover, accounting treatment methods vary subtly depending on the industry, business model, and management strategy.

Therefore, concepts alone cannot fully interpret the meaning of numbers in financial statements.

For example, Hyundai Engineering & Construction, Coupang, and Megastudy all have different ways of recognizing revenue.

Gmarket and Coupang are both e-commerce platforms, but analyzing their sales using the same criteria can lead to significant misunderstandings.

Samsung Electronics has capitalized 0 won out of its R&D expenses, but Hyundai Motor Company has capitalized over 1 trillion won.

In this way, even a single number reflects the company's choice and the characteristics of the industry.

Financial statements can't be explained with a simple formula like, "High debt means poor performance." Why did investors cheer when SK Hynix's debt surged to nearly 3 trillion won? What is the significance of the over 10 trillion won in borrowings in Samsung Electronics' financial statements? When analyzing financial statements, it's important to understand the background and context behind the numbers, not just the numbers themselves.

Numbers are easily misinterpreted without understanding the accounting context.

SK Hynix, Hyundai Motors, Coupang, Smilegate, Today's House, etc.

Let's unfold the actual financial statements and interpret the 'language of money'!

When it comes to understanding accounting in context, there's no better teaching tool than real-world examples.

The authors' over 100 case studies from business settings illustrate the vivid realities of the intertwining of accounting and management.

Rather than proceeding from theory to case studies, this book begins with issues that have arisen in the field and then works its way back to the accounting implications.

For example, we trace the accounting context by asking questions such as, “Why did this company handle expenses this way?” and “What trace did this M&A leave on the financial statements?”

The new accounting standards (K-IFRS 18) will be fully implemented starting in 2027.

Following K-IFRS 18 will bring significant changes to the income statements of listed companies.

Kakao posted an operating profit of 460.8 billion won based on its 2023 consolidated income statement.

However, if Kakao were to settle its accounts under K-IFRS 18, its operating profit would turn into a deficit of 1.4214 trillion won! This book is the first accounting book to comprehensively analyze K-IFRS 18, which will revolutionize operating profit calculations.

When you study accounting through examples, numbers become stories, not codes.

Accounting is not simply a record-keeping tool; it shows the interactions between businesses, markets, capital, and people.

Reading financial statements well means understanding the context in which the numbers were created.

When we can read accounting as a story, we finally gain the ability to see through the 'flow of money'.

***

- As Toolgen's stock price rises due to ○○, its income statement worsens.

- Why did shareholders rejoice when SK Hynix's debt soared to 2 trillion won?

- What is the 'asset under construction' that appears in the ledger of Studio Dragon, the drama production company?

- Why is Hyundai Motor Company's capitalized R&D expenses over 1 trillion won, but Samsung Electronics' capitalized R&D expenses are 0 won?

- What is the true nature of the over 10 trillion won in debt on Samsung Electronics' financial statements?

- How did Rhinos miss out on billions of won in listing profits right before his eyes?

- Today's House's current ratio is 224.8% under K-GAAP, but why is it only 39.7% under K-IFRS?

- If K-IFRS 18 is applied, why would Kakao's performance change from an operating profit of KRW 460.8 billion to an operating loss of KRW 1.4214 trillion?

Practical Accounting Class: Learning through Case Studies

"Even though I studied accounting, why am I still left with only question marks when I look at financial statements?" This book begins with that very question.

For those who are still stuck in their accounting studies despite having studied them for years, the authors of "I Almost Got to Work Without Knowing Accounting Again!", which countless readers have chosen as the "accounting book of my life," have taken up their pens again.

This time, it's not about theories, but about 'practical accounting' that applies directly to the field.

The reason we often fail at interpreting financial statements is because we miss the 'accounting context' hidden behind the numbers.

Financial statements are not simply tables of numbers.

It contains the company's strategy, management's judgment, and market changes.

Moreover, accounting treatment methods vary subtly depending on the industry, business model, and management strategy.

Therefore, concepts alone cannot fully interpret the meaning of numbers in financial statements.

For example, Hyundai Engineering & Construction, Coupang, and Megastudy all have different ways of recognizing revenue.

Gmarket and Coupang are both e-commerce platforms, but analyzing their sales using the same criteria can lead to significant misunderstandings.

Samsung Electronics has capitalized 0 won out of its R&D expenses, but Hyundai Motor Company has capitalized over 1 trillion won.

In this way, even a single number reflects the company's choice and the characteristics of the industry.

Financial statements can't be explained with a simple formula like, "High debt means poor performance." Why did investors cheer when SK Hynix's debt surged to nearly 3 trillion won? What is the significance of the over 10 trillion won in borrowings in Samsung Electronics' financial statements? When analyzing financial statements, it's important to understand the background and context behind the numbers, not just the numbers themselves.

Numbers are easily misinterpreted without understanding the accounting context.

SK Hynix, Hyundai Motors, Coupang, Smilegate, Today's House, etc.

Let's unfold the actual financial statements and interpret the 'language of money'!

When it comes to understanding accounting in context, there's no better teaching tool than real-world examples.

The authors' over 100 case studies from business settings illustrate the vivid realities of the intertwining of accounting and management.

Rather than proceeding from theory to case studies, this book begins with issues that have arisen in the field and then works its way back to the accounting implications.

For example, we trace the accounting context by asking questions such as, “Why did this company handle expenses this way?” and “What trace did this M&A leave on the financial statements?”

The new accounting standards (K-IFRS 18) will be fully implemented starting in 2027.

Following K-IFRS 18 will bring significant changes to the income statements of listed companies.

Kakao posted an operating profit of 460.8 billion won based on its 2023 consolidated income statement.

However, if Kakao were to settle its accounts under K-IFRS 18, its operating profit would turn into a deficit of 1.4214 trillion won! This book is the first accounting book to comprehensively analyze K-IFRS 18, which will revolutionize operating profit calculations.

When you study accounting through examples, numbers become stories, not codes.

Accounting is not simply a record-keeping tool; it shows the interactions between businesses, markets, capital, and people.

Reading financial statements well means understanding the context in which the numbers were created.

When we can read accounting as a story, we finally gain the ability to see through the 'flow of money'.

***

- As Toolgen's stock price rises due to ○○, its income statement worsens.

- Why did shareholders rejoice when SK Hynix's debt soared to 2 trillion won?

- What is the 'asset under construction' that appears in the ledger of Studio Dragon, the drama production company?

- Why is Hyundai Motor Company's capitalized R&D expenses over 1 trillion won, but Samsung Electronics' capitalized R&D expenses are 0 won?

- What is the true nature of the over 10 trillion won in debt on Samsung Electronics' financial statements?

- How did Rhinos miss out on billions of won in listing profits right before his eyes?

- Today's House's current ratio is 224.8% under K-GAAP, but why is it only 39.7% under K-IFRS?

- If K-IFRS 18 is applied, why would Kakao's performance change from an operating profit of KRW 460.8 billion to an operating loss of KRW 1.4214 trillion?

GOODS SPECIFICS

- Date of issue: April 25, 2025

- Page count, weight, size: 407 pages | 172*235*30mm

- ISBN13: 9791192229607

- ISBN10: 1192229606

You may also like

카테고리

korean

korean

![ELLE 엘르 스페셜 에디션 A형 : 12월 [2025]](http://librairie.coreenne.fr/cdn/shop/files/b8e27a3de6c9538896439686c6b0e8fb.jpg?v=1766436872&width=3840)