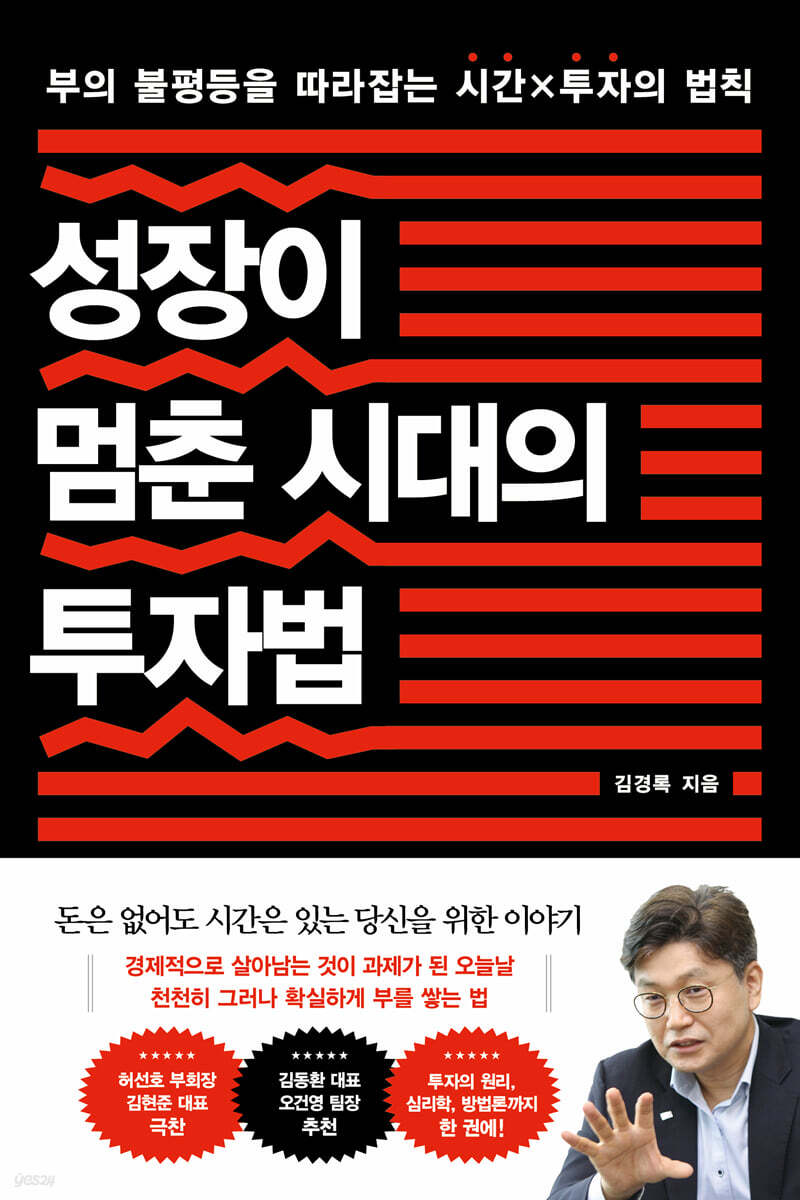

Investment in an Age of Stagnant Growth

|

Description

Book Introduction

*** It's okay if you don't have a house or an inheritance to inherit.

Build your time on the backbone of your investment.

*** Investment principles, investment psychology, and even methodology all in one book!

*** The era of low growth has arrived, where previous investment methods no longer work.

Introducing the universal rules for making money slowly but surely!

With a total fertility rate of 0.72, a rapidly shrinking working-age population, and depleted pensions… South Korea is facing the so-called “era of stagnant growth.”

We have entered a period of low growth where short-term investment methods, coin investment methods, and real estate investment methods do not work.

South Korea's economy has achieved remarkable growth over the past several decades, but demographic changes are shaking the foundations of the economy, leading to a slowdown in growth.

As the proportion of the elderly population increases dramatically compared to the productive population, the population structure is reaching the point of collapse.

Recognizing the bleak future ahead, with the driving force behind this economic growth weakening, young South Koreans have begun to say, “We have to run away.”

However, author Dr. Kim Kyung-rok, who has been reading the macroeconomic trends and people's lives as a retirement planning expert, investment expert, and economist for 30 years, says that there is opportunity in crisis.

I've been studying economics for over 40 years, but the economy and investment markets have always been turbulent and unpredictable.

And in the process, it has continued to grow.

Even though South Korea's growth may be slowing, the world is currently expanding and innovating.

To prevent young Koreans from fleeing the country where they have built their infrastructure, including family, friends, and jobs, the author introduces global investment methods through "Investment in an Age of Stagnant Growth."

Author Kim Kyung-rok is currently an advisor at Mirae Asset Global Investments, and has served as the director of Mirae Asset Retirement Research Institute, managing director of Mirae Asset Global Investments, and CIO of Mirae Asset Global Investments Chaewon Management. He has also lectured on retirement asset management to executives of major domestic companies.

However, in today's South Korea, where economic survival has become a challenge, we are publishing "Investment Methods in an Age of Stagnant Growth" to help young people with many years left to live invest.

If you're a young person just starting out in investing, or someone determined to grow your assets, this book will teach you the fundamentals of investing in an era of low growth.

Build your time on the backbone of your investment.

*** Investment principles, investment psychology, and even methodology all in one book!

*** The era of low growth has arrived, where previous investment methods no longer work.

Introducing the universal rules for making money slowly but surely!

With a total fertility rate of 0.72, a rapidly shrinking working-age population, and depleted pensions… South Korea is facing the so-called “era of stagnant growth.”

We have entered a period of low growth where short-term investment methods, coin investment methods, and real estate investment methods do not work.

South Korea's economy has achieved remarkable growth over the past several decades, but demographic changes are shaking the foundations of the economy, leading to a slowdown in growth.

As the proportion of the elderly population increases dramatically compared to the productive population, the population structure is reaching the point of collapse.

Recognizing the bleak future ahead, with the driving force behind this economic growth weakening, young South Koreans have begun to say, “We have to run away.”

However, author Dr. Kim Kyung-rok, who has been reading the macroeconomic trends and people's lives as a retirement planning expert, investment expert, and economist for 30 years, says that there is opportunity in crisis.

I've been studying economics for over 40 years, but the economy and investment markets have always been turbulent and unpredictable.

And in the process, it has continued to grow.

Even though South Korea's growth may be slowing, the world is currently expanding and innovating.

To prevent young Koreans from fleeing the country where they have built their infrastructure, including family, friends, and jobs, the author introduces global investment methods through "Investment in an Age of Stagnant Growth."

Author Kim Kyung-rok is currently an advisor at Mirae Asset Global Investments, and has served as the director of Mirae Asset Retirement Research Institute, managing director of Mirae Asset Global Investments, and CIO of Mirae Asset Global Investments Chaewon Management. He has also lectured on retirement asset management to executives of major domestic companies.

However, in today's South Korea, where economic survival has become a challenge, we are publishing "Investment Methods in an Age of Stagnant Growth" to help young people with many years left to live invest.

If you're a young person just starting out in investing, or someone determined to grow your assets, this book will teach you the fundamentals of investing in an era of low growth.

- You can preview some of the book's contents.

Preview

index

Prologue | How to Make Money Slowly but Surely

Chapter 1.

In an era of stagnant growth, are our assets safe?

The last 20 years should be forgotten.

The Path of Japanese Painting: Falling Like Cherry Blossoms and Shattered Like a Jade Sword

The Path to Koreanization: A Society of Demographic Collapse

The inflection point is around 2040.

Move the habitat of your assets

Chapter 2.

The principle of making money

If you fold a piece of paper 50 times, how high will it be?

How to Catch Up with Wealth Inequality

The Compound Interest Effect of a Monthly Investment of 500,000 Won

The Transformed FIRE Tribe vs. the Pension Saving Tribe: People at the Two Extremes

Chapter 3.

Deposits or capital, what's your choice?

Good and Bad Assets According to Warren Buffett

The most important question is, what is capital?

Isn't it okay to have a high interest deposit?

The 3 Secrets of Wealth

Why You Need Quality Global Capital

Chapter 4.

Invest in patterns, not random ones

-50%+100%=0%?

Investing is Multiplication, Not Addition: Arithmetic Mean and Geometric Mean

Investment return = Compound annual return (CAGR) = Geometric mean return

Take advantage of volatility

Taming the Goddess of Fate

Life is random and patterned.

Chapter 5.

Dispersion, dispersion, it's dispersion in the end

How to reduce the risk of marriage?

Spatial distribution: straw sandal vendor and wooden clog vendor

Time Diversification: Why More People Make Money in Real Estate Than Stocks

Fixed-Amount Investment: Invest as if saving a fixed amount.

The fault lies with me, not the market.

Chapter 6.

The Psychology of Investing

We are made vulnerable to investment

Dr. Jekyll and Mr. Hyde inside me

The utility you get from money is more important than the money itself.

Loss hurts twice as much as gain.

Rule of thumb bias: the law of small numbers, anchors, and availability

Motivational biases: confirmation bias, optimism, and overconfidence

People who make high-risk, low-return investments

overreaction

Chapter 7.

Lifetime asset management to prepare for a life of deficit

Why Humans Live Longer Than Tigers

Characteristics of Lifetime Asset Management

Are you a stock or a bond?

Two Puzzle Stories

Three risks faced during withdrawal

Product distribution when earned income is zero

Chapter 8.

Behind a diligent worker stands a pension.

The cornerstone and safety net of life

Pension sets you free

Pension! You need to know it.

Six Tax Benefits of Pensions

Bundle, Invest, and Pensionize

What if I lose money on my pension investment?

Can South Korea's default option save old age?

Chapter 9.

The first problems you will encounter

Create seed money and invest?

House or stocks?

Good debt, bad debt

A perspective on bankruptcy

The Key to Asset Allocation for Maximum Returns

Traditional Assets: Characteristics of Stocks and Bonds

Alternative Assets: Characteristics of Absolute Return, Real Assets, and Private Equity

Asset allocation implementation

Chapter 10.

Use financial products

Funds, the basics of asset management products

Rapidly growing ETFs

The S&P 500 index represents 70 years of American corporate history.

REITs Investment Method

How to Use the Default Option for Retirement Pensions

TDF is a lifetime automatic asset allocation fund.

ELS is not a medium-risk, medium-return product.

What follows when assets go overseas?

Epilogue

Americas

Chapter 1.

In an era of stagnant growth, are our assets safe?

The last 20 years should be forgotten.

The Path of Japanese Painting: Falling Like Cherry Blossoms and Shattered Like a Jade Sword

The Path to Koreanization: A Society of Demographic Collapse

The inflection point is around 2040.

Move the habitat of your assets

Chapter 2.

The principle of making money

If you fold a piece of paper 50 times, how high will it be?

How to Catch Up with Wealth Inequality

The Compound Interest Effect of a Monthly Investment of 500,000 Won

The Transformed FIRE Tribe vs. the Pension Saving Tribe: People at the Two Extremes

Chapter 3.

Deposits or capital, what's your choice?

Good and Bad Assets According to Warren Buffett

The most important question is, what is capital?

Isn't it okay to have a high interest deposit?

The 3 Secrets of Wealth

Why You Need Quality Global Capital

Chapter 4.

Invest in patterns, not random ones

-50%+100%=0%?

Investing is Multiplication, Not Addition: Arithmetic Mean and Geometric Mean

Investment return = Compound annual return (CAGR) = Geometric mean return

Take advantage of volatility

Taming the Goddess of Fate

Life is random and patterned.

Chapter 5.

Dispersion, dispersion, it's dispersion in the end

How to reduce the risk of marriage?

Spatial distribution: straw sandal vendor and wooden clog vendor

Time Diversification: Why More People Make Money in Real Estate Than Stocks

Fixed-Amount Investment: Invest as if saving a fixed amount.

The fault lies with me, not the market.

Chapter 6.

The Psychology of Investing

We are made vulnerable to investment

Dr. Jekyll and Mr. Hyde inside me

The utility you get from money is more important than the money itself.

Loss hurts twice as much as gain.

Rule of thumb bias: the law of small numbers, anchors, and availability

Motivational biases: confirmation bias, optimism, and overconfidence

People who make high-risk, low-return investments

overreaction

Chapter 7.

Lifetime asset management to prepare for a life of deficit

Why Humans Live Longer Than Tigers

Characteristics of Lifetime Asset Management

Are you a stock or a bond?

Two Puzzle Stories

Three risks faced during withdrawal

Product distribution when earned income is zero

Chapter 8.

Behind a diligent worker stands a pension.

The cornerstone and safety net of life

Pension sets you free

Pension! You need to know it.

Six Tax Benefits of Pensions

Bundle, Invest, and Pensionize

What if I lose money on my pension investment?

Can South Korea's default option save old age?

Chapter 9.

The first problems you will encounter

Create seed money and invest?

House or stocks?

Good debt, bad debt

A perspective on bankruptcy

The Key to Asset Allocation for Maximum Returns

Traditional Assets: Characteristics of Stocks and Bonds

Alternative Assets: Characteristics of Absolute Return, Real Assets, and Private Equity

Asset allocation implementation

Chapter 10.

Use financial products

Funds, the basics of asset management products

Rapidly growing ETFs

The S&P 500 index represents 70 years of American corporate history.

REITs Investment Method

How to Use the Default Option for Retirement Pensions

TDF is a lifetime automatic asset allocation fund.

ELS is not a medium-risk, medium-return product.

What follows when assets go overseas?

Epilogue

Americas

Detailed image

Into the book

After chatting with young people, I decided to write an investment theory book that was 'very easy to understand but didn't miss the principles.'

In addition, I tried to write "Investment Theory" in a way that is consistent with the author's logic, but also in a way that is easy for anyone to understand the principles of money growth.

Burton Malkiel said, “Investing is about making money slowly but surely.”

There is nothing to add or subtract from this definition.

What I pursued in this book is 'how to make money slowly but surely'.

--- p.8, from “There are principles to follow in investing”

- People who manage assets must prepare for various possibilities.

Will the apartment republic that flourished during the period of rapid growth continue into a prolonged period of low growth? Will we be able to compete with advanced economies with the local currency, the won? As the pyramid-shaped population structure flips, will our economy achieve a soft landing or collapse? (…) During periods of shrinking populations and abnormal demographic imbalances, even a small factor could send our economy into a tailspin.

Based on predictions based on population structure changes, our economy is expected to face a fierce battle around 2040.

--- p.12, from “You don’t have to leave this land, just move the habitat of your assets”

- We are aging at the fastest rate in the world.

Thus, 50 years later, the elderly dependency ratio will be the highest among OECD countries.

(…) We need to move our assets to young, innovative places.

Where will you place your assets? And how will you manage them? Proper asset management is now your survival.

--- p.51, from “Moving the Habitat of Assets”

- The annual return of the S&P 500, the representative composite stock index in the United States, is 10%.

But don't underestimate 10%.

If you manage 100 million won with compound interest for 20 years, it becomes 670 million won.

If we operate here for another 10 years? Don't be surprised.

It amounts to 1.745 billion won.

The principal of 100 million won has become over 1.7 billion won after 30 years.

In this way, welfare gives blessings to those who have endured well for a long time.

--- p.59, from “How high will the paper be if folded 50 times?”

- If you want to manage your assets to prepare for the 100-year lifespan, it is best to start early.

Even if the money is small, it's good.

A little money makes up for it in time.

As the early bird catches the worm, those who prepare early will enjoy a peaceful old age.

Remember, the secret is not to buy assets that will rise rapidly in the short term, but to start early and buy time.

--- p.61, from “How high will the paper be if folded 50 times?”

- Stocks and real estate are called capital.

Deposits are not considered capital.

'What is the fundamental difference between deposits and capital?' (...) Many people answer with answers like, 'Deposits are safe,' 'Deposits preserve the principal,' and 'Deposits pay a fixed interest rate.'

That's right.

Most people consider principal preservation to be a huge advantage of deposits.

However, there is no increase in the principal amount of deposits.

Therefore, it is more correct to define deposits as assets whose value does not change rather than as assets that preserve the principal.

(…) So, is an asset whose price does not change a good asset?

--- p.84, from “The Most Important Story: What is Capital?”

- There are two brothers, a straw sandal seller and a wooden sandal seller.

There are two seasons in a year, rainy and dry, and the straw sandal vendor earns -25% during the rainy season and 50% during the dry season.

On the other hand, the straw sandal seller earns 50% during the rainy season and -25% during the dry season.

A mother is always worried about her two children.

When it rains, I worry about the straw sandal seller's son, and when it's sunny, I worry about the straw sandal seller's son.

How can these two brothers ease their mother's worries, reduce business volatility, and live better lives? The answer is for the two brothers to exchange half of their shares.

--- p.135, from “Spatial Dispersion: Straw Sandal Seller and Wooden Clog Seller”

- The key to successful investing begins with knowing yourself.

I need to know how to take in information and make decisions when investing.

I need to know whether I easily make decisions based on stock market rumors and why I do so.

This chapter is somewhat unfamiliar.

The reason I am introducing it is because, in order to not get lost in the battlefield-like investment market, you must keep cognitive 'bias' in mind.

What are cognitive biases in investing, how do they arise, and how can we overcome them?

--- p.157, from “The Psychology of Investment”

- Life is not a fantasy world.

Life itself is like walking on a bumpy road.

If we are not careful, our lives in old age could collapse in the 100-year lifespan.

If you buy some stocks as assets after retirement, you cannot rule out the possibility that the stock price will suddenly plummet by 25% like in 1987.

Is that all?

You may live 20 years longer than you expected, or face severe inflation.

In old age, you are helpless against rising prices because you do not have income or assets that rise as much as prices.

Therefore, life asset management requires a more sophisticated and detailed model.

--- p.199, from “Life Asset Management to Prepare for a Life in the Red”

- When talking to young people about asset management, I've been asked, "Do you save your seed money safely in deposits?"

(…) Seed money is money needed to buy a house or start a business, but it is not needed in the process of accumulating assets.

Moreover, it makes no sense to save up seed money in the beginning and then invest in stocks or other investments once you have the money.

It is not about first preparing seed money through deposits and then connecting the lump sum to investments.

Savings should be directly linked to investment.

--- p.275, from “Creating seed money and investing?”

- Real estate is a reliable alternative asset that can protect against inflation.

People have to live somewhere, and even as the population declines, new people continue to move into cities.

This means there is a stable demand base.

Peter Lynch, the legendary stock fund manager, once offered some interesting insights into the merits of investing in housing, saying, “Buy a house before you buy stocks.”

In addition, I tried to write "Investment Theory" in a way that is consistent with the author's logic, but also in a way that is easy for anyone to understand the principles of money growth.

Burton Malkiel said, “Investing is about making money slowly but surely.”

There is nothing to add or subtract from this definition.

What I pursued in this book is 'how to make money slowly but surely'.

--- p.8, from “There are principles to follow in investing”

- People who manage assets must prepare for various possibilities.

Will the apartment republic that flourished during the period of rapid growth continue into a prolonged period of low growth? Will we be able to compete with advanced economies with the local currency, the won? As the pyramid-shaped population structure flips, will our economy achieve a soft landing or collapse? (…) During periods of shrinking populations and abnormal demographic imbalances, even a small factor could send our economy into a tailspin.

Based on predictions based on population structure changes, our economy is expected to face a fierce battle around 2040.

--- p.12, from “You don’t have to leave this land, just move the habitat of your assets”

- We are aging at the fastest rate in the world.

Thus, 50 years later, the elderly dependency ratio will be the highest among OECD countries.

(…) We need to move our assets to young, innovative places.

Where will you place your assets? And how will you manage them? Proper asset management is now your survival.

--- p.51, from “Moving the Habitat of Assets”

- The annual return of the S&P 500, the representative composite stock index in the United States, is 10%.

But don't underestimate 10%.

If you manage 100 million won with compound interest for 20 years, it becomes 670 million won.

If we operate here for another 10 years? Don't be surprised.

It amounts to 1.745 billion won.

The principal of 100 million won has become over 1.7 billion won after 30 years.

In this way, welfare gives blessings to those who have endured well for a long time.

--- p.59, from “How high will the paper be if folded 50 times?”

- If you want to manage your assets to prepare for the 100-year lifespan, it is best to start early.

Even if the money is small, it's good.

A little money makes up for it in time.

As the early bird catches the worm, those who prepare early will enjoy a peaceful old age.

Remember, the secret is not to buy assets that will rise rapidly in the short term, but to start early and buy time.

--- p.61, from “How high will the paper be if folded 50 times?”

- Stocks and real estate are called capital.

Deposits are not considered capital.

'What is the fundamental difference between deposits and capital?' (...) Many people answer with answers like, 'Deposits are safe,' 'Deposits preserve the principal,' and 'Deposits pay a fixed interest rate.'

That's right.

Most people consider principal preservation to be a huge advantage of deposits.

However, there is no increase in the principal amount of deposits.

Therefore, it is more correct to define deposits as assets whose value does not change rather than as assets that preserve the principal.

(…) So, is an asset whose price does not change a good asset?

--- p.84, from “The Most Important Story: What is Capital?”

- There are two brothers, a straw sandal seller and a wooden sandal seller.

There are two seasons in a year, rainy and dry, and the straw sandal vendor earns -25% during the rainy season and 50% during the dry season.

On the other hand, the straw sandal seller earns 50% during the rainy season and -25% during the dry season.

A mother is always worried about her two children.

When it rains, I worry about the straw sandal seller's son, and when it's sunny, I worry about the straw sandal seller's son.

How can these two brothers ease their mother's worries, reduce business volatility, and live better lives? The answer is for the two brothers to exchange half of their shares.

--- p.135, from “Spatial Dispersion: Straw Sandal Seller and Wooden Clog Seller”

- The key to successful investing begins with knowing yourself.

I need to know how to take in information and make decisions when investing.

I need to know whether I easily make decisions based on stock market rumors and why I do so.

This chapter is somewhat unfamiliar.

The reason I am introducing it is because, in order to not get lost in the battlefield-like investment market, you must keep cognitive 'bias' in mind.

What are cognitive biases in investing, how do they arise, and how can we overcome them?

--- p.157, from “The Psychology of Investment”

- Life is not a fantasy world.

Life itself is like walking on a bumpy road.

If we are not careful, our lives in old age could collapse in the 100-year lifespan.

If you buy some stocks as assets after retirement, you cannot rule out the possibility that the stock price will suddenly plummet by 25% like in 1987.

Is that all?

You may live 20 years longer than you expected, or face severe inflation.

In old age, you are helpless against rising prices because you do not have income or assets that rise as much as prices.

Therefore, life asset management requires a more sophisticated and detailed model.

--- p.199, from “Life Asset Management to Prepare for a Life in the Red”

- When talking to young people about asset management, I've been asked, "Do you save your seed money safely in deposits?"

(…) Seed money is money needed to buy a house or start a business, but it is not needed in the process of accumulating assets.

Moreover, it makes no sense to save up seed money in the beginning and then invest in stocks or other investments once you have the money.

It is not about first preparing seed money through deposits and then connecting the lump sum to investments.

Savings should be directly linked to investment.

--- p.275, from “Creating seed money and investing?”

- Real estate is a reliable alternative asset that can protect against inflation.

People have to live somewhere, and even as the population declines, new people continue to move into cities.

This means there is a stable demand base.

Peter Lynch, the legendary stock fund manager, once offered some interesting insights into the merits of investing in housing, saying, “Buy a house before you buy stocks.”

--- p.276, from “House or Stocks?”

Publisher's Review

Having many days to live is a blessing

How to make money slowly but surely

While the legal retirement age is 60 and life expectancy is estimated at 120 years, there are concerns that South Korea's pension system is running out.

According to the National Pension Service's financial projections, the National Pension Service's reserves will be completely depleted by 2055.

And over the next 10 years after 2040, the total number of households will decrease by more than 1 million.

In addition, the stock market capitalization is expected to decline after 2035, and total financial assets will also experience their first decline after peaking in 2040.

Now, for those who have no house, no inheritance, or no property to inherit, surviving 'economically' in old age has become a challenge in itself.

However, in "Investing in an Age of Stagnant Growth," the author tells a story of investment where having many days to live is a blessing.

The center of the story is definitely 'time'.

“The proven principles of making money in the investment market so far are ‘compound interest,’ ‘long-term,’ and ‘volatility.’

You need to maximize the compounding effect to make money, and to maximize the compounding effect, you need to manage your savings, rate of return, and investment period well.

Just as a nation needs time to accumulate for growth, so too does making money require time to accumulate.” _From the text

“If you want to manage your assets to prepare for the 100-year lifespan, it is best to start as soon as possible.

Even if the money is small, it's okay.

“A little money makes up for the time.” _From the text

It is said that a chick considers the first person it sees after breaking out of the egg to be its mother.

For those who see a coin dominating the market, the idea of making a lot of money in a short period of time takes hold.

In a market where real estate investors thrive, real estate is seen as a shortcut to wealth.

However, there are universal laws in investment that have been proven by many people, and South Korea has entered a period of low growth.

It does not work through previous investment methods.

This book contains the principles of successful investment suitable for the low-growth era, which have survived countless objections.

We introduce “an investment theory that is very easy but doesn’t miss the principle” so that everyone can understand the principle of money multiplication and become rich.

The driving force of the Earth is gravity, and the driving force of capitalist society is capital.

A story about how anyone can become rich by using 'capital'.

The 2008 global financial crisis broke out.

Our country's stock prices also fell sharply.

But at this time, a huge money spree occurred in the United States.

The policy called quantitative easing was also implemented to draw the sword before the social dynamics of the United States stopped.

In this way, the driving force of capitalist society is ‘capital.’

“All systems are focused on capital investment, production, and compensation.” And the natural and fastest way to become rich is to utilize ‘capital.’

So what exactly is capital? "Investing in an Age of Stagnant Growth" presents methods for utilizing capital, assets that produce output.

It persuasively presents, with proven data, the "optimal savings amount" that maximizes the compounding effect, the principle of capital growth, and the "minimum rate of return" to enjoy the compounding effect, and the "period of time" during which assets should be accumulated.

Even a small amount per month is fine.

Anyone can become wealthy by building large assets through savings, returns, and investment periods.

Living in a random world, there is only one task left.

Dispersion Dispersion is ultimately dispersion

Investing isn't about simply leaving it to chance; it's about analyzing market patterns and managing volatility.

Everything in the world is random.

The movements of the world are unpredictable.

But if you look at it from a distance, everything follows a pattern.

The world and the investment market are the same.

Therefore, the key to successful investing is finding a way to generate stable profits in a volatile market.

“If you invest in the US S&P 500 for one year, the returns will fluctuate significantly, but if the investment period exceeds 10 years, the volatility will converge within a certain range.

Randomness is patterned.

The key to the investment market is finding this pattern.

Although there have been many attempts to find patterns, this chapter explores some commonly accepted methods.

Options, spatial diversification, time diversification, and accumulated investment.” _From the text

"Investing in an Age of Stagnant Growth" teaches investment methods that reduce volatility through "diversification."

By diversifying your investments across various sectors, time periods, and savings plans, you can reduce risk and achieve stable returns.

Even if you don't get a so-called jackpot return by investing like this, it will give you the average return that the stock market offers.

And if that average rate of return continues, it will give you a higher return than concentrated investment.

After retirement, your earned income becomes zero and you enter a life of deficit where you only spend money.

But behind every honest worker, there is a pension!

Pension Experts Explain Pension and Investment Principles

When a tiger gets old and loses its teeth and claws, it dies.

But people live a rich and leisurely life even as they grow older.

What is the difference between a tiger and a human?

It is 'money'.

People have created a system to survive when they cannot work, using money as a currency.

In addition, they receive support from their children and sometimes receive assistance from the state through social contracts.

“If money is a means for individuals to manage their own retirement, filial piety is a device for family members to take responsibility for their own retirement, and old-age pension is the state’s involvement in an individual’s retirement.” However, this pattern is beginning to change in our country.

Due to low birth rates and an aging population, the number of children to support has decreased, while parents' life expectancy has increased.

In addition, the pyramid-shaped population structure, in which the productive population supported the elderly population, is changing to an inverted pyramid shape.

“We need to raise enough money from a small number of young people to provide pensions to a large number of old people,” but this is realistically difficult.

Ultimately, the time has come for individuals to prepare for life asset management on their own.

After retirement, when your earned income becomes zero, withdrawals become constant.

You need to use the assets you accumulate in your youth to generate the income you need after retirement.

The countermeasure for this period is ‘pension’.

Pensions are the cornerstone and safety net of retirement life.

"Investment in an Age of Stagnant Growth" analyzes Korea's pension system, dividing it into national security, corporate security, individual security, and housing security. It presents specific plans for Korean workers to gradually save and manage their earned income to prepare for retirement through basic pension, public pension, retirement pension, pension savings, pension insurance, and housing pension.

It fully embodies the principles of pension investment for Korean office workers.

How to make money slowly but surely

While the legal retirement age is 60 and life expectancy is estimated at 120 years, there are concerns that South Korea's pension system is running out.

According to the National Pension Service's financial projections, the National Pension Service's reserves will be completely depleted by 2055.

And over the next 10 years after 2040, the total number of households will decrease by more than 1 million.

In addition, the stock market capitalization is expected to decline after 2035, and total financial assets will also experience their first decline after peaking in 2040.

Now, for those who have no house, no inheritance, or no property to inherit, surviving 'economically' in old age has become a challenge in itself.

However, in "Investing in an Age of Stagnant Growth," the author tells a story of investment where having many days to live is a blessing.

The center of the story is definitely 'time'.

“The proven principles of making money in the investment market so far are ‘compound interest,’ ‘long-term,’ and ‘volatility.’

You need to maximize the compounding effect to make money, and to maximize the compounding effect, you need to manage your savings, rate of return, and investment period well.

Just as a nation needs time to accumulate for growth, so too does making money require time to accumulate.” _From the text

“If you want to manage your assets to prepare for the 100-year lifespan, it is best to start as soon as possible.

Even if the money is small, it's okay.

“A little money makes up for the time.” _From the text

It is said that a chick considers the first person it sees after breaking out of the egg to be its mother.

For those who see a coin dominating the market, the idea of making a lot of money in a short period of time takes hold.

In a market where real estate investors thrive, real estate is seen as a shortcut to wealth.

However, there are universal laws in investment that have been proven by many people, and South Korea has entered a period of low growth.

It does not work through previous investment methods.

This book contains the principles of successful investment suitable for the low-growth era, which have survived countless objections.

We introduce “an investment theory that is very easy but doesn’t miss the principle” so that everyone can understand the principle of money multiplication and become rich.

The driving force of the Earth is gravity, and the driving force of capitalist society is capital.

A story about how anyone can become rich by using 'capital'.

The 2008 global financial crisis broke out.

Our country's stock prices also fell sharply.

But at this time, a huge money spree occurred in the United States.

The policy called quantitative easing was also implemented to draw the sword before the social dynamics of the United States stopped.

In this way, the driving force of capitalist society is ‘capital.’

“All systems are focused on capital investment, production, and compensation.” And the natural and fastest way to become rich is to utilize ‘capital.’

So what exactly is capital? "Investing in an Age of Stagnant Growth" presents methods for utilizing capital, assets that produce output.

It persuasively presents, with proven data, the "optimal savings amount" that maximizes the compounding effect, the principle of capital growth, and the "minimum rate of return" to enjoy the compounding effect, and the "period of time" during which assets should be accumulated.

Even a small amount per month is fine.

Anyone can become wealthy by building large assets through savings, returns, and investment periods.

Living in a random world, there is only one task left.

Dispersion Dispersion is ultimately dispersion

Investing isn't about simply leaving it to chance; it's about analyzing market patterns and managing volatility.

Everything in the world is random.

The movements of the world are unpredictable.

But if you look at it from a distance, everything follows a pattern.

The world and the investment market are the same.

Therefore, the key to successful investing is finding a way to generate stable profits in a volatile market.

“If you invest in the US S&P 500 for one year, the returns will fluctuate significantly, but if the investment period exceeds 10 years, the volatility will converge within a certain range.

Randomness is patterned.

The key to the investment market is finding this pattern.

Although there have been many attempts to find patterns, this chapter explores some commonly accepted methods.

Options, spatial diversification, time diversification, and accumulated investment.” _From the text

"Investing in an Age of Stagnant Growth" teaches investment methods that reduce volatility through "diversification."

By diversifying your investments across various sectors, time periods, and savings plans, you can reduce risk and achieve stable returns.

Even if you don't get a so-called jackpot return by investing like this, it will give you the average return that the stock market offers.

And if that average rate of return continues, it will give you a higher return than concentrated investment.

After retirement, your earned income becomes zero and you enter a life of deficit where you only spend money.

But behind every honest worker, there is a pension!

Pension Experts Explain Pension and Investment Principles

When a tiger gets old and loses its teeth and claws, it dies.

But people live a rich and leisurely life even as they grow older.

What is the difference between a tiger and a human?

It is 'money'.

People have created a system to survive when they cannot work, using money as a currency.

In addition, they receive support from their children and sometimes receive assistance from the state through social contracts.

“If money is a means for individuals to manage their own retirement, filial piety is a device for family members to take responsibility for their own retirement, and old-age pension is the state’s involvement in an individual’s retirement.” However, this pattern is beginning to change in our country.

Due to low birth rates and an aging population, the number of children to support has decreased, while parents' life expectancy has increased.

In addition, the pyramid-shaped population structure, in which the productive population supported the elderly population, is changing to an inverted pyramid shape.

“We need to raise enough money from a small number of young people to provide pensions to a large number of old people,” but this is realistically difficult.

Ultimately, the time has come for individuals to prepare for life asset management on their own.

After retirement, when your earned income becomes zero, withdrawals become constant.

You need to use the assets you accumulate in your youth to generate the income you need after retirement.

The countermeasure for this period is ‘pension’.

Pensions are the cornerstone and safety net of retirement life.

"Investment in an Age of Stagnant Growth" analyzes Korea's pension system, dividing it into national security, corporate security, individual security, and housing security. It presents specific plans for Korean workers to gradually save and manage their earned income to prepare for retirement through basic pension, public pension, retirement pension, pension savings, pension insurance, and housing pension.

It fully embodies the principles of pension investment for Korean office workers.

GOODS SPECIFICS

- Date of issue: August 19, 2024

- Page count, weight, size: 360 pages | 452g | 140*210*30mm

- ISBN13: 9788965966425

- ISBN10: 8965966426

You may also like

카테고리

korean

korean

![GQ KOREA Mark (Monthly): December [2025]](http://librairie.coreenne.fr/cdn/shop/files/8ef265dbbfbf186523ed75ba7319009d.jpg?v=1765340328&width=3840)